Six weeks to solve the crisis. That was George Osborne's stark warning last Friday, after world stock markets had been battered by fears that the world is heading for a new recession.

Three days later, and the clock is ticking. Last night, high-level talks in Washington DC between top finance ministers and International Monetary Fund officials broke up without any clear signs of a deal. There is talk of creating a €2tn warchest to rescue Europe's struggling countries, but no clear idea how this will happen.

Financial markets will give their verdict on the Washington talks today – the early reaction from Asia has not been favourable, with most markets falling sharply. Investors in London are predicting more losses here too – but trading is likely to be volatile.

We'll bring you all the key developments in the European debt crisis today. Let us know what you think too, below the line…

European stock markets have just opened - with another bout of heavy selling. The FTSE 100 index fell by 92 points, sending the blue-chip index slumping back through the 5,000 point mark to 4974 points.

Mining companies are the biggest fallers in the City, driven by those fears of a global slowdown and the recent falls in commodity prices.

There are similar falls in other European markets – the French CAC fell 2% at the open, with Germany's DAX down 1.3%.

That looks like a pretty vigorous thumbs-down to the Washington DC talks, and the failure to develop a solid plan to end the turmoil.

Far Eastern markets have also suffered today. Some markets are still trading, but right now every one is down on the day -- this round-up of the Asian markets is splattered with red electronic ink.

Japan's Nikkei has closed at its lowest level since April 2009. It tumbled by 186 points, or 2.17%, to 8,374.13.

The worst performer is the Jakarta Composite index, which is down 5.5% today in late trading. Indonesia's exports trade is dependent on natural resources – a global slowdown will erode demand for products such as oil, gas and coal.

You might think that the prospect of a €2trn warchest to save the eurozone would spark a rally in shares, rather than another early selloff. The reason, it appears, is that many in the City aren't convinced that the plan can be put together, having witnessed months of bickering and indecision among Europe's leaders.

Michael Hewson, market analyst at CMC Markets, was encouraged that EU leaders are preparing to enlarge their current bailout fund, along with talk of recapitalising Europe's banks and guiding Greece into an "orderly default". However, he warns that the plan will probably need to be approved by every eurozone member – which is the reason that the "Save Greece" agreement hammered out on 21 July still hasn't been approved.

Hewson is also disappointed by the latest pronouncements from the leaders closest to the situation:

Markets are likely to remain sceptical while EU officials continue to utter contradictory statements – with ECB member and Bank of France governor Christian Noyer stating that there was no need for a recapitalisation of French banks.

German chancellor Angela Merkel also added to the uncertainty with mixed messages on German TV last night as she continued to walk a fine line with the German voters, saying that a euro area insolvency cannot be ruled out, and at the same time saying that Greece cannot be allowed to default.

We've also seen a startling plunge in the price of gold and silver this morning.

The spot price of gold tumbled to as low as $1,534 per ounce this morning, a fall of more than $100 per ounce. Back on 6 September, it was trading above the $1,900 mark.

Silver was even more badly hit – slumping from $31.04 per ounce to just $26.04 per ounce. That's a 16% drop in value, in just a few hours' trading.

There are three reasons for today's sharp falls:

• The US dollar has strengthened overnight, which typically pushes down the price of assets priced in dollars. Despite America's own debt issues, investors can't break the habit of treating the greenback as the Safe Haven par excellence

• There's also a general 'dash for cash', as firms sell their precious metal assets to raise funds to cover losses elsewhere

• The upfront cost of trading in both metals has just risen, with CME Group raising the cash deposit it demands from traders who buy gold and silver futures. That should deter speculators, and may encourage them to quit the gold market.

The latest healthcheck of Germany's business sector, the IFO index, has been just released – and it's not exactly good news.

Confidence in Germany fell for the third month running, with IFO's business climate index (a measure of optimism, or otherwise) hitting 107.5 in September. That shows the situation has darkened compared with a month ago, when confidence took its biggest dive since the collapse of Lehman Brothers.

However, it is better than economists had expected (the consensus forecast was for 106.5).

The euro has strengthened against the dollar, to $1.343 (from as low as $1.3364 earlier). Stock markets are also clawing their way back, with the FTSE 100 now down just 9 points at 5057.

But the survey also paints a worrying picture of the situation in Europe's biggest economy. It warns that businesses are sceptical about future prospects, with the global economy clearly cooling. IFO advises industrial producers to "shift down a gear" – another sign that the slowdown is here.

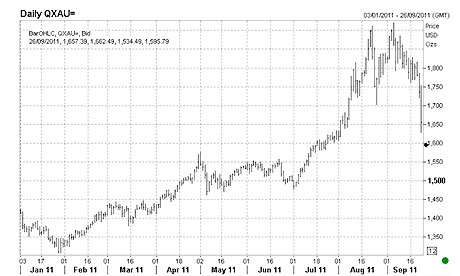

The gold price has recovered some of today's early losses (spot gold is now $1,617 per ounce, down nearly $50 today). But as this graph shows, the charge towards $2,000 per ounce has been rudely interrupted in the last three weeks.

The spot gold price during 2011. Photograph: Reuters

The spot gold price during 2011. Photograph: Reuters

The $300 slump in the spot gold price since 6 September (when it hit $1,920/oz) is sweet music to the ears of those who argue that gold is a bubble ripe for popping.

FT journalist Alan Beattie, for example, has been entertainingly tweeting on this subject this morning. Beattie was criticised by political blogger Guido Fawkes earlier this month for supporting Gordon Brown's infamous sale of the UK gold reserves. It sounds like he's enjoying the recent change of fortune:

@alanbeattie: The respective treacheries of Gordon Brown and George Osborne are inversely related & the ratio calibrated by the gold price #goldbuglogic

@alanbeattie: Propose permanent ticker on ft.com showing how much G Osborne is robbing Britain by failure to short gold at peak. #goldbugs

Beattie also worked out that the chancellor could have bought every UK citizen an iPod Shuffle if he'd dumped Britain's entire gold reserves on the market when spot gold hit that record high of $1,920/oz..

JP Morgan's banking experts have been analysing how Europe's banking sector could be propped up, allowing it to absorb future sovereign debt losses.

They conclude that up to €148bn of fresh capital may have to be injected, in a scheme dubbed "Euro TARP" – in a nod to the America's Troubled Asset Relief Programme of 2008.

"Euro-TARP is in our view the best risk-reward medicine for opening the Eurobank funding market," said analyst Kian Abouhossein, in a note sent to JP Morgan's clients.

Abouhossein's calculations are based on the assumption that Europe's banks will have to take haircuts (losses) of 60% on Greek sovereign debt, 40% on bonds issued by Portugal and Ireland and 20% on Italy and Spain's debts.

How would the capital be injected? Abouhossein reckons EU governments will pick "mandatory convertibles", a kind of bond that automatically converts into shares in the future.

European stock markets have made a remarkable recovery. After falling nearly 100 points at the start of trading, the FTSE 100 index is now sitting on a healthy 40-point gain.

And it's not exactly clear why. Financial stocks are certainly looking healthier, with Barclays (154.2p) , Royal Bank of Scotland (21.56p) and Lloyds Banking Group (35.9p) all up by more than 5% right now.

That's despite few serious developments this morning, but some interesting pronouncements from European policymakers (of which more shortly).

Ben Critchley, sales trader at IG Index, reckons that the City has grown a little bit more confident that a credible rescue plan will be implemented (but this may not last long!):

The casual observer could be forgiven for thinking it's been a calm start to the day, with the FTSE trading around 30 points higher. However, the first couple of hours have already seen a 100 point-plus range for the index, as traders weigh up the implications of the latest words from EU leaders.

For now at least, it looks as if markets are giving some credence to a firm plan on how to tackle the debt crisis beginning to emerge – but if recent experience is anything to go by, this patience is unlikely to last too long if details are not forthcoming.

I wonder if there really are many "casual observers" right now. Everywhere we turn, we see grim warnings that a new depression is imminent. For example, Bill Jamieson in the Scotsman yesterday:

For the atmosphere now is ominously akin to 1931 and the chain of events unleashed by the collapse of Credit-Anstalt. Everything seems headed for a denouement, the final spark to a massive pile of dry kindling. All around, the atmosphere crackles with foreboding.

If you can read that without getting a little shiver, you've got better nerves than I.

We mentioned in the last post that EU officials have been talking about the crisis this morning. Two individuals stand out, both members of the European Central Bank, mainly because they appear to be at odds with each other.

Austria's Ewald Nowotny appeared to hint this morning that the ECB could cut interest rates – which would be somewhat embarrassing for the central bank, having hiked borrowing costs in April and July this year. Nowotny told news agency Market News that:

The ECB never pre-commits, and rate cuts cannot be excluded.

But fellow policymaker Yves Mersch has rubbished the suggestion that the ECB may cut rates in October, saying these "wild expectations" should be quashed. Mersch insisted that the ECB will not be distracted from its responsibility to control inflation.

Some economists argue that those two rate hikes were a mistake, especially now that stimulating economic growth is a more pressing concern than taming inflation (witness the Federal Reserve's Operation Twist, and the Bank of England's dilemma on whether, and when, to increase its own quantitative easing programme).

Looking at the UK economy briefly, one of the nine policymakers who set UK interest rates has revealed that he came close to voting for a second round of quantitative easing (QE) this month.

Ben Broadbent

Ben Broadbent

Ben Broadbent, the newest member of the monetary policy committee, told a Reuters event this morning that he came "reasonably close" to voting for more QE (in the event, poor Adam Posen was again left standing alone).

Broadbent said that "it would not take much more of a deterioration" in the economy for him to pledge more money to the Bank's QE programme (which tries to drive down borrowing costs and stimulate growth by buying corporate and government debt).

Broadbent also argued that the "international environment is clearly disinflationary" – a sign that rate rises are off the agenda.

Howard Archer of IHS Global Insight reckons the Bank will crack the champagne bottle on the side of QE2 within six weeks:

We currently expect the Bank of England to announce a further £50bn of Quantitative Easing by November, taking the stock up to £250bn.

While we currently favour a move in November, it is very possible that the Bank could act at the conclusion of the 5-6 October MPC meeting if UK data over the next couple of weeks show further weakness and the global economic environment fails to show any signs of improvement.

My colleague Phillip Inman has been analysing Ben Broadbent's speech this morning (see last post for more). He says Broadbent launched a spirited defence of the Bank's approach to monetary policy, which has seen inflation run well ahead of target throughout 2011.

More from Phillip:

Ben Broadbent, the Goldman Sachs economist who joined the Bank of England's monetary policy committee in the summer, has leapt to the defence of the Bank's inflation policy and in particular the stance of the Bank's boss Mervyn King.

In a speech this morning to City bankers, he said tackling inflation through higher interest rates during last year and this would only have pushed up unemployment and depressed demand even further.

With total real value of wages across the economy declining anyway, Broadbent argues that it is better for everyone to share the pain via higher inflation, rather than some people suffering though even higher unemployment.

And here's the key quote from Broadbent:

Even credible monetary policy has its limits. The long rise in commodity prices, the financial crisis and the sluggish rebalancing of supply have all acted to reduce real household incomes. It matters to some degree whether this occurs via higher inflation or lower nominal wages, because the latter route would probably have involved higher unemployment, if only for a time.Credibility means monetary policy can, within limits, choose the former course. But the hit to real incomes would have occurred either way.

Over on FT Alphaville, Neil Hume has perhaps the best explanation for why the stock markets are enjoying a small revival (FTSE 100 now up 58 points at 5119, clawing back some of the tens of billions "wiped off" the index late last week).

As Neil pithily explains, the Footsie was:

"Down 90 points first thing, on disappointment that the IMF had come up with nothing concrete. Then we all decided they [had] sketched out a plan that might work, but it will take six weeks to knock together...so we can all relax for a bit, and have a punt."

Our own Nick Fletcher warns that there is "likely to be a lot more volatility" before any European rescue deal is agreed, with banks and insurers topping the leaderboard at present.

Josh Raymond of City Index agrees that the current mini-rally may lack a certain solidity:

Naturally there are some investors who are adding shares to their portfolios on speculation that the rescue plan leaked over the weekend to effectively top up the EFSF to €2 trillion may trigger a bounce back...

It may however be a bit optimistic at this stage for investors to buy into stocks believing that we could see a similar stock market rally to that which followed the last massive rescue plan that was announced at the 2009 G20 meeting in London.

Then the FTSE 100 rallied some 60% over the next two years, though this time around, we could be looking not only at a leveraged top up of the EFSF but a recapitalising of the major banks and a large haircut of Greek debt, which might make the immediate consequences and the processes that would allow for such an action much more clouded.

World leaders need to take immediate action to avoid a "massive jobs shortfall" next year, the respected International Labour Organisation has warned.

With G20 employment ministers gathering in Paris today, the ILO has calculated that 20 million jobs have been lost since the financial crisis began in 2008. At the current rate of job creation, there is no chance of recreating these lost positions by 2015. In fact, should employment rates slow further, the shortfall could double to 40 million.

"We must act now to reverse the slow-down in employment growth and make up for the jobs lost," warned ILO director-general Juan Somaviaw warned.

In Italy, shares have jumped on optimism that European banks will be recapitalised. The main index, the FTSE MIB, has jumped by more than 4% today.

The Italian banks are surging ahead - with Intesa Sanpaolo rising by 11.3%, and UniCredit up 9%. Intesa Sanpaolo's shares were briefly suspended, such was the rush of buy orders.

The rally appears to also be driven by hopes of a European Central Bank rate cut, even though policymaker Yves Mersch rubbished the idea earlier today.

All this volatility can't be good for nerves in the City - where Steve Collins, head of dealing at London & Capital Asset Management, is dreaming of a future without stock markets:

@TradeDesk_Steve: I SUPPOSE ONCE EVERYTHING IS NATIONALISED WE WONT HAVE TO WORRY ABOUT EQUITY PRICE MOVES LIKE THIS

Not, of course, that many governments have the spare cash for a massive asset-buying programme. The Square Mile is safe for a while yet.

Time for a round-up of developments thus far:

• A volatile morning on Europe's stock markets as investors try to weigh up whether Europe will put together a €2 trillion rescue package

• FTSE 100 is up by 51 points at 1pm at 5118, while Italy's main market leaps 4%. The Nikkei, though, closed at its lowest level since April 2009

• Gold and silver slide again – with spot gold now down by $300/oz since 6 September

• European Central Bank policymakers appear divided over wisdom of cutting interest rates, as Bank of England MPC member hints at more QE soon

Are Europe's leaders really on the same page? One of the three elements* of the €2 trillion (some say €3 trillion) rescue plan outlined by EU officials in Washington over the weekend is a significant cut in Greece's debts – with a 50% haircut being widely reported.

Greek finance minister Evangelos Venizelos, though, has denied that any such plan is being considered. Here's a quote from a statement just issued by Greece's finance ministry:

We have reached a point where there are reports about what has been said in a closed door meeting with the participation of only Mrs [Christine] Lagarde, Mr [Jean-Claude] Trichet and myself.

What is absolutely sure is that there hasn't been, and couldn't have been, any discussions about the so-called scenario of an orderly default.

The yield on Greece's two-year government bonds is currently around 85%, a level where a default is pretty well 'priced in'. If any orderly default wasn't even discussed, what exactly did Venizelos, Trichet and Lagarde chat about?

* - the other two elements being

i) recapitalising the European banking sector, which JP Morgan believes could cost up to €148bn

ii) massively enlarging the power of the €440bn European Financial Stability Fund

Louise Cooper, markets analyst at BGC Partners, is also irked by the lack of unity among the European political elite. She writes:

The Greek finance minister was quoted yesterday suggesting no to default, the French budget minster Valerie Pecresse said no recapitalisation is planned for French banks. Oh dear.

We are back to the failure of the eurozone political class to acknowledge the scale of the problem and the required response.

Cooper harks back to 2008, when US treasury secretary Hank Paulson apparently broke the deadlock over America's bank rescue package by kneeling in front of Nancy Pelosi (then House Speaker) to beg for her party's support for the bailout plan.

Maybe we need that again, a Master of the Universe humiliating himself in front of a politician to illustrate the depth of the problem? Any suggestions as to who should get on bended knee to Angela Merkel would be welcome...

Suggestions are most welcome, in fact! I don't think we have a prize, but the glory of the wittiest answer could be yours, so get posting. It'll pass the time until Wall Street opens, anyway.

Incidentally, the Paulson-Pelosi anecdote is in Too Big To Fail, Andrew Ross-Sorkin's gripping account of the financial crisis of 2008. Highly recommended.

A poll of Greek citizens has found that a majority of people vehemently oppose leaving the eurozone. Helena Smith, our correspondent in Athens, has more details:

In findings that will hearten the EU, the main provider of rescue funds for the debt-stricken nation, 66 percent of Greeks are against a return to the drachma believing it would aggravate their fiscal woes, according to the Public Issue poll published in the authoritative Sunday Kathimerini.

The poll showed that two years after the debt crisis erupted, the majority of Greeks who wanted to remain in the euro zone were those most affected by stringent austerity measures demanded in exchange for aid by the country's "troika" of lenders, the EU, International Monetary Fund and European Central Bank.

Support for the euro had increased by five percentage points since May when 58 percent of Greeks said they were in favour of retaining the euro.

But in a sign that Greeks no longer believe what their politicians say, 60% said they thought the country was heading for sovereign default. Finance minister Evangelos Venizelos has categorically denied that Athens will soon be unable to manage a debt load that at 360 billion euro and climbing has surpassed all projections. The IMF's original forecast that the debt pile would peak at 160 percent of GDP in 2012 was modified upwards last week to 189 percent of GDP.

Helena adds that a review of Greece's fiscal progress is expected to be completed this week when a mission of top Troika experts arrive in Athens to decide whether to give Greece its sixth tranche of aid, worth €8bn. Without it, George Papandreou's cash-strapped government has admitted it will be unable to pay public sector wages and pension in October.

So Graeme is now taking his leave for the day so I, Jill Treanor, am taking over. So we are just marking time now until the US opens.

So Wall Street is flat at the open, the Dow Jones index is up just 1.97 points - 0.02% - at 10,773. The broader measure of the market - the S&P 500 - is doing a bit better, rising 1%. In London, the FTSE 100 is up 21 points at 5,086.

Now, it seems as if the Dow Jones might indeed have been a bit higher at the start. The index is now up 1% after a "technical problem" stopped "real-time dissemination" of prices. In these sort of markets, such technical problems are not welcome.

Well stock markets are negative now. Looks as if the focus is now back on the "recession story" after the latest data from the US on new home sales, which reached a record low at the end of August. The number of homes for sale in the US at the end of August were 162,000 - a record low - compared with 164,000 in July.

The latest up date on the state of eurozone economies comes from our economics correspondent, Phillip Inman.

Portugal has stayed under the radar during the Greek/Italy crisis, but according to a survey of the property market, remains in a parlous state.

The August Rics/Ci Portuguese Housing Market Survey (PHMS) shows deterioration in market conditions since July.

The national activity and national confidence indices fell by 8 and 2 points respectively to -33 and -51, while the national price balance fell from -55 to -59, said Rics.

At its heart, Portugal suffers from a chronic lack of demand. The major cities of Lisbon and Porto saw the steepest declines, while foreign buyers kept the declines along the Algarve more modest.

Even an almost complete moratorium on building has had little effect.

Rics said developers selling the few new properties on the market fared better than residential agents trying to offload second homes.

Rics senior economist, Josh Miller says: "In Portugal, it is the demand side of the equation that is weighing down on prices, with the double digit unemployment rate feeding through to weakness in new buyer enquiries.

Miller put a positive gloss on Portugal's lack of new developments dating back to the boom years.

"Unlike in Spain and Ireland, oversupply is not an issue; the official statistics show no evidence of overbuilding prior to the economic downturn and new vendor instructions have been falling all year. Consequently, once the economy starts to recover, Portugal will not have to cope with the residential inventory issue that other countries face."

As I write, the FTSE 100 is in positive territory although only just. Up 2 points!

Earlier today, Graeme was writing about the gold price and the dramatic fall it is suffering after the big rally that took place during the summer. The economists at Capital Economics are highlighting the action on the gold price today too.

Our relatively pessimistic diagnosis of the outlook for the global economy and for the euro-zone in particular is being proved right. The market fall-out has been much as we had anticipated too, including steep falls in the prices of equities and industrial commodities, much lower yields on high-grade government debt, including US Treasuries, and a partial recovery in the dollar.

Nonetheless, one thing we had not anticipated was the slump in the price of gold, which has fallen by more than $300 from the record nominal high of $1921 per ounce recorded on 6 September. Two of the pillars that supported the long bull market in gold have recently been knocked away, namely the fears of a surge in inflation and a collapse in the dollar. However, other pillars remain strong, including the outlook for monetary policy and the prospect of a re-escalation of the crisis in the euro-zone.

What's more, the fundamentals that support gold's status as a safe haven have not changed in the last few days. Above all, gold's value does not depend on the creditworthiness of any government or financial institution, and that may yet prove very significant in the weeks ahead. If fears of a break-up of the euro-zone really take hold, gold is still likely to benefit more than any other currency, even if the dollar proves to be the best of the rest.

In part this is because the upside for the gold price is not constrained by broader economic and policy considerations in the same way as the value of the dollar. Confidence in the dollar relative to gold is also likely to be undermined again by the fall-out from fresh euro-zone shocks on the US economy and banks.

So, in the last 25 minutes or so before the FTSE 100 closes, an update arrives from Michael Hewson, market analyst at CMC Markets.

After opening lower the main European benchmarks have seen downside tempered by talk out of Europe about the consideration of bank recapitalisations, a 50% Greek default and an increase of leveraging up of the bailout fund (EFSF).

Uncertainty remains the predominant sentiment, however as European markets trade in predominantly positive territory, however the resource heavy FTSE100 is finding it difficult to sustain much in the way of gains due to weakness in mining stocks.

He describes the euro as having had a "fairly choppy day" as it hit fresh seven month lows against the US dollar and 10 year lows against the yen. But talk about a plan to recapitalise Europe's banks - which has been circling for day - helped the single currency rebound.

While we wait for the FTSE 100 to close, our correspondent on Wall Street, Dominic Rushe, provides the following analysis of the latest developments in the US.

Wall Street started well but then lost steam and – shock horror – it might actually not have anything to do with the Greeks.

The Dow Jones Industrial Average rose by triple digits in early trading. Encouraging news following it's biggest weekly point drop since October 2008. Then it started sliding back. An analysts report that Apple had cut Asian orders from iPad parts by 25% rattled investors. The story looks a lot less worrying now – sounds like those orders are just going to Brazil rather than indicating anything more sinister.

So, the FTSE 100 is closed now. And after something of a yo-yo session, has ended in positive territory, up 22.56 at 5089.37. But that 0.4% rise in London, is not as big as the rises experienced in Germany, France and Spain where the main stock market indices were up 2.8%, 1.9% and 2.6% respectively amid hopes that some sort of deal can be done among eurozone leaders to build a firewall around a Greece.

While the markets seem to think a default is a possibility, political leaders seem to be denying that such an outcome is being considered. A bit like the constant chatter about a bailout for the French bank sector.

Jon Peace, top banks analyst at Nomura, notes that the Banque de France governor Christian Noyer has not ruled the possibility of French banks using the support measures put in place for the country's banks during the 2008 crisis when up to €360bn was made available to French banks.

Peace said:

French bank shares rallied strongly last Friday on growing optimism for government support in a repeat of 2008. In that year, as late as October 14 the major French banks were denying the need for new capital amid market concerns about solvency. Less than one week

later on October 20 the French government announced a €10.5bn recapitalisation plan.

Research arrives from economists at Barclays Capital outlining a cut to their forecasts for UK GDP.

We have cut our forecast of GDP growth in the second half of 2011 and first half of 2012, but nudged up our forecast for the sector half of 2012.

They are now forecasting GDP growth of 0.2% quarter-on-quarter in the third and fourth quarters of this year, revised down from 0.5% and 0.3% previously.

Our assessment is that underlying growth is approximately zero, with some unwinding of the temporary factors that lowered output in Q2 lifting growth to 0.2% quarter-on-quarter.

Louise Cooper of BGC provides me with a good note on which to end. She is pointing out the volatility in the markets: a 15% swing in the price of Deutsche Bank today, for instance, while the main index in Germany - the DAX - has moved 6% and the main index in France - the CAC- also moved 6% from peak to trough today. She says

These are extreme moves in equity markets and show the massive uncertainty that we face. What will the Eurozone look like in the future? Answers on a postcard please..

As I sign off in London, Wall Street is now up 157 points. Again optimism about a solution to the eurozone crisis is cited as a reason for the gains. Wall Street's close, though, is still four hours away.... Answers on a postcard, as Cooper would say, as to where the index will close.