Good morning. After lively trading on Wall Street on Tuesday - the Dow Jones was down about 2% but surged 4% in the last hour of trading to close 1.4% higher at 10808.71, a gain of 153 points - the FTSE 100 index in London is expected to open 60-70 points higher. On Tuesday US shares rallied on news that EU finance ministers were examining ways of co-ordinating recapitalisations of financial institutions.

Not all Asian markets followed Wall Street's lead, however. Japan's Nikkei slid 0.86% to 8382.98 while Hong Kong's Hang Seng lost 3.4% to 16,250.27.

Dampening any euphoria over EU plans to shore up banks, Moody's downgraded Italy by three notches last night, to A2 from Aa2 with a negative outlook - giving Italian bonds a lower rating than Estonia and putting them on a par with Malta. The credit ratings agency said it saw a "material increase" in funding risks for highly indebted eurozone countries, and warned of possible further downgrades.

"The negative outlook reflects ongoing economic and financial risks in Italy and in the euro area," Moody's said in a statement. "The uncertain market environment and the risk of further deterioration in investor sentiment could constrain the country's access to the public debt markets."

Michael Hewson market analyst at CMC Markets explains:

The fluidity of the situation in Europe was aptly illustrated last night in the space of a fraught sixty minutes with stocks rallying sharply on reports that European finance ministers were examining ways of co-ordinating large scale recapitalisations of banks on a local level in an attempt to convince markets that governments would do all they could to safeguard and support the European banking sector.

Just as they market had begun to digest that little nugget, ratings agency Moody's with impeccable timing finally delivered on its ratings downgrade for Italy, downgrading them three notches to A2, with a negative outlook, citing increased risk in long term funding as well as increased downside risks to economic growth and to fiscal consolidation.

The FTSE has opened 120 points higher at 5064, a 2.4% gain, as markets digest the EU bank plan.

There was also some reassuring news on troubled Franco-Belgian bank Dexia this morning. The French finance minister Francois Baroin said "tomorrow a solution should be found". He added that Dexia could not stay in its current form. "It's indisputable," he said on RTL radio. He also said a solution involving French state-owned banks Caisse des Dépôts and Banque Postale, the finance arm of its postal service, would be the most "solid".

Meanwhile, the Belgian caretaker prime minister Yves Leterme said nationalisation of Dexia's Belgian activities was one possibility being considered.

Later this morning markets will be looking at the key UK services PMI data for September, which is expected to slip back from August's 51.1 to 50.6. It's out at 9.30am London time. At the same time, the Office for National Statistics will be releasing its annual "Blue Book". New methodology will mean massive revisions to past GDP data, while the final estimate for the second quarter is expected to be reaffirmed at GDP growth of 0.2%. No doubt the figures will give the Bank of England's monetary policy committee plenty of food for thought when it starts its two-day meeting today.

And Greece faces a general strike.

Here's more on the EU bank plan. Gary Jenkins, head of fixed income at Evolution Securities, sums it up:

The markets are not so much driven by fear and greed nowadays as they are by hope and despair. For most of yesterday the latter had the upper hand with further concerns about the European banks leading equity markets sharply lower; the Eurostoxx 50 closed down 2.21% and the FTSE 100 was down 2.58%. However the last hour of US trading saw a remarkable turnaround as the S&P 500 gained 4% to close up 2.25% on the day. This was on the back of an FT story that European finance ministers discussed the need to recapitalise Europe's banks at yesterday's meeting.

Olli Rehn said "There is an increasingly shared view that we need a concerted, co-ordinated approach in Europe……there is a sense of urgency….capital positions of European banks must be reinforced to provide additional safety margins and thus reduce uncertainty…". Note however that there has been "no formal decision" to commence a co-ordinated recapitalisation of the banks...

The recapitalisation of banks is a fine idea, but if the politicians could solve the sovereign crisis that would go a long way to solving the banking crisis. Recapitalising the banks would be positive and it would no doubt help risk assets in the short term. But it would not solve the sovereign problems and thus unless the EU is happy to just keep buying Italian bonds (via the ECB / EFSF) then at some stage the market will focus on the sovereigns rather than the banks.

Shares in Dexia have leapt nearly 10% to €1.106, after the French finance minister promised a rescue by Thursday, while Bank of France governor Christian Noyer said the central banks of France and Belgium would ensure the troubled lender has enough liquidity.

The FTSE is still up over 100 points at 5045, a 2% gain. Barclays is the biggest riser, up 7.6% at 151.9p, followed by miners Rio Tinto, Eurasian, BHP Billiton, Cairn Energy, Kazakhmys and Xstrata. Oil, which fell below $100 a barrel on Tuesday, is back up over $100.

Here are Tuesday's comments on shoring up the banks from Olli Rehn, European commissioner for economic affairs, in full. He spoke to the Financial Times.

There is an increasingly shared view that we need a concerted, co-ordinated approach in Europe while many of the elements are done in the member states. There is a sense of urgency among ministers and we need to move on.

Capital positions of European banks must be reinforced to provide additional safety margins and thus reduce uncertainty. This should be regarded as an integral part of the EU's comprehensive strategy to restore confidence and overcome the crisis.

This is what is happening today.

• 9.30am UK services PMI; European services PMIs

• 9.30am The UK Blue Book with massive revisions to past GDP data

• Bank of England's two-day monetary policy committee meeting begins

• 3pm US ISM manufacturing

• General strike in Greece

In Greece, airlines have been grounded, trains halted and tax offices shut as public workers walked out to protest against the government's harsh austerity measures - defying the prime minister's plea to rally behind its effort to fend off the country's bankruptcy. Hospitals ran on emergency staff and state schools shut in the first nationwide strike since the summer lull. In Athens' airport, more than 400 domestic and international flights were cancelled, Reuters reported.

The country's unions expect hundreds of thousands of people to strike. "Unfortunately the new measures are just extending the unfair and barbaric policies which suck dry workers' rights and revenues and push the economy deeper into recession and debt," Stathis Anestis, spokesman for the GSEE union told Reuters. "With this strike, the government, the EU and the IMF will be forced to reconsider these disastrous policies."

The FTSE is now only up 60 points at 5005, a 1.2% gain.

The PMI services surveys for the eurozone paint a troubling picture. Italy's services sector has shrunk at its sharpest pace for more than two years, and rather worryingly, Germany's service industries have slipped into contraction territory for the first time since July 2009, with the index falling to 49.7 in September from 51.1 in August. Italy's PMI dropped to 45.8 from 48.4, the lowest since July 2009, and Spain also posted its weakest reading since then, with the PMI at 44.8, indicating a sharper contraction.

In the eurozone as a whole, the services sector has worsened with the index falling to 48.8, which indicates a faster contraction than previously. The UK PMI will be released at 9.30am and is expected to show services still expanded last month, albeit at a weaker pace.

Here is some reaction to the eurozone services PMIs from Howard Archer, chief UK and European economist at IHS Global Insight.

Eurozone service sector activity contracted for the first time in 25 months in September according to the purchasing managers, and at a deeper rate than first reported. Furthermore, the deterioration was widespread in September, with Germany seeing the first contraction in services activity since July 2009 and French expansion slowing sharply to a 25-month low. Worryingly, there was deeper services contraction in both Spain and Italy, adding to the concerns over their economy. Ireland bucked the trend, seeing marginally faster expansion.

Contraction in the Eurozone's key services sector during September, coupled with a marked decline in new business, heightens concern that the Eurozone could be heading back into recession and puts pressure on the ECB to cut interest rates as soon as Thursday.

Indeed, with manufacturing activity contracting in September for a second month running, Markit's composite output indicator for the two sectors sank to 49.1 from 50.7 in August, thereby indicating overall contraction in services and manufacturing output for the first time since July 2009.

Eurozone economic activity is clearly being held back by tighter fiscal policy increasingly kicking in across the region, squeezed consumer spending power and the major hit to confidence coming from the heightened Eurozone sovereign debt tensions and global financial market turmoil. Also critically, slower global growth is now hitting foreign demand for Eurozone goods and services hard.

Furthermore, falling prices charged in the services and manufacturing sectors combined in September supports the view that Eurozone consumer price inflation will soon head downwards on a sustainable basis despite spiking up to 3.0% in September.

While an ECB interest rate cut is a possibility on Thursday, latest comments by policymakers suggest that it is more likely than not that the central bank will keep interest rate at 1.50% for now. Indeed, there was no hint of a rate cut on Thursday from ECB President Jean-Claude Trichet when he addressed the European Parliament earlier this week.

The euro slipped on Wednesday, hovering near a nine-month low against the dollar, as investors grew more sceptical over EU finance ministers' willingness to act quickly to beef up the banks. It was trading at $1.3290 after hitting $1.3260 earlier.

Kasper Kirkegaar, currency strategist at Danske Bank in Copenhagen, told Reuters:

At this point, there's just been news of discussions about possible bank recapitalisations, there's no details yet. There's a high risk of a further sell-off if we don't get details on this soon.

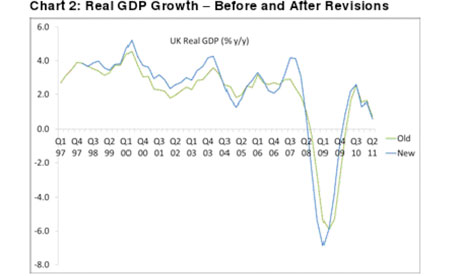

Alas, we had some technical problems just as the Office for National Statistics published revised GDP figures. In a surprise revision, it said the UK economy grew by just 0.1% in the second quarter, less than the 0.2% previously estimated. This is the slowest quarterly growth rate since the end of last year, when the economy contracted by 0.5%.

"We've had some new data in, but the majority of the change is due to new methods and some new industrial weights," a statistician said.

It turns out Britain's 2008-09 recession was shorter but deeper than previously thought. After changing its methodology, the ONS carried out a major recalculation of its historical data and now reckons the slump was 7.1% from peak to trough, rather than 6.4%.

And we've had another surprise, this time a positive one. The UK service industries bucked the worsening European trend and improved last month, with the PMI rebounding from August's eight-month low to 52.9 in September. The FTSE is now up 90 points at 5035, an 1.84% increase.

Jonathan Loynes, chief European economist at Capital Economics, can't get very excited about the bounceback in Britain's service industries, and reckons the Bank of England should pump more money into the economy. He says:

Coupled with the equivalent indices of the construction and manufacturing reports, this points to GDP growth of about 0.1% per quarter – positive at least. However, the average reading in Q3 as a whole suggests that GDP may well have fallen during the quarter. Meanwhile, the national accounts give a very downbeat picture of the economy's past performance. Not only was growth nudged down in Q2 (from +0.2% q/q to +0.1%), but revisions to the back data left a bigger drop in output during the recession (7.1%) than previously estimated (6.4%). This would seem to contradict recent suggestions that there might be less spare capacity in the economy than previously thought. Overall, further justification for the MPC to launch QE2 either tomorrow or next month.

Here is ING economist James Knightley's take on the improvement in Britain's services sector.

Today's report shows the biggest rise in the headline index since March. It is possible that the PMIs were negatively affected by concerns over the August riots and now the fears of wider civil unrest have faded the surveys are recovering. Indeed, the global macro backdrop continues to deteriorate and the expectations component of the index fell to its lowest level sine March 2009 - the depths of the recession. Consequently we believe it is only a matter of time before we see more QE.

We favour November as the announcement point for more QE from the BoE given close proximity to the Fed and ECB policy meetings and the Cannes G20 summit. Being seen to act in some kind of coordinated fashion may also give the stimulus "more bang for its buck" rather than going it alone currently in what are very volatile markets and a mixed environment for data. With the Fed consistently highlighting that QE2 was less effective than QE1 in the US we suspect QE2 in the UK will amount to around an extra £300bn of asset purchases. This would bring the total spend to half a trillion pounds.

We set up this Flickr group during our Greek Week coverage, and invite any readers in Greece to share images of how the general strike today is affecting them.

More on the UK growth numbers. Alan Clarke, of Scotia Bank, says:

GDP revisions. Source: Scotia Capital/ONS Photograph: Scotia Capital/ONS

The Office for National Statistics has rewritten history. UK GDP data back to 1997 has been revised. At the margins, growth has been revised up. Most importantly, the upward revisions to the recent growth data that the Bank of England had been banking on failed to materialise – rather there were slight downward revisions! The downward revision to Q2 growth to just 0.1% q/q was disappointing. Given that surveys have weakened since Q2, there is an increasing chance of negative GDP at some point during H2.

My colleague Helena Smith in Athens has the latest on the general strike there.

Greeks workers have decided that today's strike is the "beginning of a battle" against measures that are not only described as barbaric but as having pushed people to the brink of penury. The waft of angry chants from the thousands of demonstrators who have taken to the streets can be heard throughout the centre of Athens.

"They are asking us to accept reforms that were carried out in England by Thatcher over the course of several years in a matter of weeks ... it's very violent, we're not going to take it sitting down," said Tatianna Karayianni at the civil servants' union Adedy. This is the first general strike since the beleaguered Greek government announced the imposition of a hugely unpopular property tax and lay-offs in the public sector - belt-tightening that has added to the sense of bewilderment and shock now shared by a growing number of austerity-weary Greeks.

It's a beautiful autumnal day in Athens but everyone is now waiting to see if violence will win the day when protestors rally outside parliament in the hours ahead.

There are some IMF headlines coming out just now. Antonio Borges, head of the European Department of the IMF, says European banks need between €100 and €200bn to recapitalise. He says the problems in the European banking sector need immediate attention and banks need more capital to restore confidence in them.

The TUC says the latest GDP figures show a double-dip recession is now a real danger. Its general secretary Brendan Barber says:

The economic news just keeps on getting worse. Today's revision of the GDP growth figures show the economy is doing even more badly than expected. There is now a real danger of the UK going back into recession, and the best that current policies can deliver will be years of stagnation.

We need action to kick start the economy, rather than speeches telling us to look on the bright side. The fall in household spending is almost as steep as at the height of the crash as wages are squeezed, prices rise and families cut back.

Of course people should be sensible about paying back unsustainable debt, but the truth is that the government is relying on people borrowing more as OBR forecasts reveal. George Osborne must be hoping that people ignore the Prime Minister's advice to pay back their credit cards today.

Here is an update on the situation in Greece, where thousands of striking workers marched to the parliament to protest against the government's austerity measures. Riot police have fired teargas at a small group of rock-throwing youths on the central Syntagma Square in the Greek capital, according to Reuters.

The comments from the IMF are interesting because they also suggest that they are willing to create a special purpose vehicle, alongside the EFSF bailout fund, to buy Italian and Spanish bonds.

Divyang Shah at Thomson Reuters writes:

This is important stuff as until now the focus has been on eurozone guaranteed money coming via the EFSF but the involvement of the IMF as another layer in the equity tranche to help support Italy and Spain provides an added protective barrier for potential investors.

Of these potential investors we had Japan overnight suggest that they are willing to buy more EFSF bonds beyond the 20% purchase they already make. There is even the chance that the IMF may play a larger role in leveraging the EFSF should markets worry that there are not enough funds for the EFSF to be effectively leveraged given that not much the €440bn has already been committed.

Time for a lunchtime round-up of today's news.

• The FTSE is up 113 points at 5057, a 2.3% gain

• Britain's 2008-09 recession was shorter, but deeper than previously thought, and the UK grew by just 0.1% in the second quarter (rather than 0.2%)

• The UK's service industries bounced back in September, while in the eurozone, things have taken a turn for the worse

• In Greece, public workers have embarked on a general strike

Returning to the issue of shoring up European banks, here are Charles Jenkins' thoughts. He is an economist at the Economist Intelligence Unit.

The proposed concerted action to recapitalise banks is much later than it should be but is still welcome. Although it will not solve the problems of the more vulnerable countries an admission that there are difficulties also in the stronger countries and that remedial action needs to be co-ordinated should help to give more of a feeling that all euro zone countries are in difficulty together because of the imbalances between them rather than always pointing the finger at the weaker ones.

Ed Balls MP, Labour's shadow chancellor, said in response to today's revised growth figures:

These deeply concerning figures show the British economy has stagnated since the autumn of last year, well before the eurozone crisis. They should set alarm bells ringing in Downing Street and the Treasury. They show things are even worse than we thought and that the economy has not grown at all for nine months.

It is deeply out of touch for Ministers to claim Britain is a safe haven when our recovery was choked off last autumn, well before the problems in the eurozone and global markets of recent months.

David Cameron and George Osborne urgently need to realise that spending cuts and tax rises which go too far and too fast have hit consumer confidence, killed the recovery and pushed up unemployment. This will just make it harder and harder to get the deficit down and the government is already set to borrow £46 billion more because of slower growth and higher unemployment.

As today's figures show families struggling with higher food and energy prices, rising unemployment and the VAT rise are already struggling to get by and cutting back. They don't need an out of touch Prime Minister lecturing them about paying off their credit cards.

What they do need is a Prime Minister and Chancellor with the strength to realise their plan is hurting but not working. There is a better way and Labour has set out a clear five point plan to create jobs, help struggling families and support small businesses. I hope that in his speech this afternoon David Cameron adopts one or more of these measures. He needs to come up with a plan for jobs and growth and he needs to do it fast.

Hello everyone. This is Alex Hawkes taking over briefly from Julia Kollewe.

And the news at lunchtime is...a little mixed. Two separate US jobs reports are pointing in different directions, to be precise.

Data from ADP says that US private sector employers added 91,000 jobs in September, against expectations of 75,000.

Separately we have data from consultants Challenger, Gray and Christmas, who say that the number of planned layoffs at US firms jumped in September to its highest total in two years.

Difficult to know whether to make much of either data point - but the ADP data appears to have pushed stock index futures up a little. The S&P 500 is predicted to open up 4 points later today, about 0.3%.

Are the wild swings in the markets based on anything really happening? Last night's 4% rise in the Dow and the excitable reaction of European markets this morning was apparently related to the FT's suggestion that the EC finally had a plan to recapitalise Europe's banks.

But does it have a plan? There seemed to be some non-denial denials coming out of Brussels this morning.

Regardless of that, our man in Brussels, David Gow, at least has some sense of how it all happened:

The European Commission suddenly went on the back foot today after the comments on a "plan" to recapitalise European banks given to the FT by Olli Rehn, economic and monetary affairs commissioner. First, journalists from other European and overseas media were angry that, yet again, the FT appears to be the exclusive port of call for market-sensitive news emanating from Brussels (see last night's movements on Wall St and again today in Europe). Second, in an acutely defensive and disingenuous manner, EC spokesmen had to reject accusations of special treatment - and make plain there is no plan in sight.

Giving every semblance of being overtaken by events, the EC spokesmen/women insisted that Rehn, a shy Finn, desperately wanted to give a presser after yesterday's Ecofin meeting in Luxembourg but couldn't - because the Poles, who hold the EU's six-month presidency, wanted to have a long-delayed lunch (at 1700CET) instead. In fact, the Polish presidency refused to let him upstage their finance minister.

So, Rehn, who "doesn't like giving individual interviews and much prefers press briefings," scooted off back to Brussels in a fast car to hold vital meetings. And, it so happened that the FT called during his break-neck journey up the E341 - and he spoke. Not about a "EU bank rescue plan" (FT) but "a European approach based on national efforts co-ordinated at European level." Hmm. This reporter and colleagues waiting to talk to George Osborne tried to approach Rehn and his team on Tuesday evening but they scuttled away - so he wasn't that desperate to talk apart from to the FT.

More critically than bruised journalistic egos: the EC, which is indeed meant to help co-ordinate steps to manage the crisis, is only now, very belatedly, acknowledging that the bank stress tests carried out in July have been completely overtaken by the enveloping sovereign debt crisis and the gradual freezing of inter-bank lending/borrowing. "We're aware of what's happening on the markets and the impact on European banks," was the limp response. What about comments by Antonio Borges, head of the IMF's Europe program, that European banks need €100bn-200bn in recapitalisation? "Don't want to speculate on figures of that magnitude."

More like a Berlaymont version of "Sorry But I haven't a Clue"...

Greece's recession started earlier than previously thought, and will be even deeper this year than feared.

That's the gloomy message from the Elstat statistics agency, which has just revised its historic GDP data (as the UK's Office for National Statistics did this morning). Elstat now reckons that the Greek economy has been shrinking since 2008. On the upside, the decline in 2010 was less severe than calculated before -- but that means that 2011 will probably see an even deeper retrenchment.

According to the new stats, Greece shrank by 0.2% in 2008 (rather than growing by 1%). That means the country was already retreating as Lehman Brothers collapsed.

Last year, Greece shrank by 3.5% rather than the 4.5% previously inked in. That suggests 2011 could see a 5.5% contraction, Elstat predicted. Making it even harder for Athens to meet its fiscal targets?

Here's the Elstat revisions:

2006 2007 2008 2009 2010

New +5.5 +3.0 -0.2 -3.2 -3.5

Old +5.2 +4.3 +1.0 -2.0 -4.5

Angela Merkel has just thrown her support behind a recapitalisation of Europe's banks - the issue of the day. Speaking in Brussels after a meeting with EC President Jose Manuel Barroso, the German Chancellor said Germany was prepared to pump up bank capital reserves "if it is needed'.

Photograph: Oliver Berg/Getty

Photograph: Oliver Berg/Getty

From Merkel's press conference, taking place in Brussels now:

I think it is important, if there is a general view that the banks are not sufficiently capitalised for the current market situation, that one does it.

The German government -- as the finance minister has made very clear in the last two days -- stands ready to implement such a capitalisation of the banks if it is needed.

Angela Merkel's hint that European bank recapitalisation is close has cheered the City (writes Graeme Wearden).

As has some better-than-feared economic data from the US. The monthly non-manufacturing ISM report (basically, a healthcheck of America's services industry), showed that activity only dropped slightly in September. And, encouragingly, the sector was still growing.

This has sent the FTSE 100 up by 153 points to 5098, a rise of over 3%. And on Wall Street, the Dow Jones index has clambered into positive territory after falling at the start of trading.

In normal times, a 3% swing on the Footsie would be a little remarkable. Today, though, not so much.

My colleague David Gow is at Angela Merkel's press conference in Brussels, where she signalled her support for bank recapitalisation. He points out that, highly significantly, Merkel indicated that a decision could be made in less than two weeks, on "17-18 October".

Those date are crucial for the future of the eurozone. A full EU summit is scheduled for Monday 17 October. Members of the Eurozone are planning to meet the following day (Tuesday 18th).

So Merkel may be indicating that a bank rescue deal will be hammered out at those meetings. Or maybe even before?....

While Europe is gripped by the question of how to strengthen its banking sector, the original EFSF bailout plan agreed in July is still being ratified (and looking seriously dated).

The Dutch Parliament has just announced that it will vote on the proposal to increase the EFSF to €440bn tomorrow (not next Wednesday, as previously planned).

However, Slokavia remains the pesky fly in the eurozone ointment. Its coalition government still cannot agree on a deal to approve the EFSF. The junior partner, the SaS party, opposes a larger bailout fund, with party leader Richard Sulik warning today that it could still vote against the plan.

Speaking in Bratislava this afternoon, Sulik said "he could not see a solution on the horizon" at the moment.

Out in Athens, protesters and riot police are facing off. Helena Smith has the very latest:

Units of riot police have been rushed to Syntagma Square, the plaza that faces the Greek parliament, but there are not more than a few hundred demonstrators gathered in the square.On previous occasions Syntagma resembled the Gaza Strip with protesters leaving a trail of destruction behind them ... this time the streets were filled with traffic and people were going about their business as normal, even if the whiff of anger hangs in the air ....

More as we get it

Europe's stock markets have just closed, with tens of billions of pounds being "wiped onto" share prices.

In London, the FTSE 100 finished 157 points higher, or up 3.19%, at 5102.17. However, traders aren't exactly cheering. Will Heddon of IG Index called it "Just another day in London, just another triple-digit day for the FTSE 100".

Here's more from him:

Each day we shift between hope and dismay for the eurozone, with today being a day for the former. The IMF has said they will back a second bailout for Greece, and thus we have our 'hope' box ticked. Yesterday's EU statement that they would help aid bank liquidity if necessary has not been given any concrete foundations as of yet, but it has at least been reiterated by the German government.

Don't expect this to be the end of it. Now this sets us up nicely for tomorrow's ECB rate announcement, now widely expected to be unchanged, and this despite poor eurozone data this week.

Other European markets also surged today. The German Dax and the French Cac finished 4.7% and 4.3% up respectively.

Breaking news from my colleague and banking expert Jill Treanor -- she reports that "senior heads" will be rolling at UBS very shortly, connected to the the alleged rogue trading of Kweku Adoboli.

Jill will have more details very soon, over at our business blog.

Capital Economics is warning that a European bank recapitalisation programme might backfire, and spark a new sovereign debt crisis.

Why? Because forcing Greek bondholders to accept a bigger cut on their debts would be seen as a dangerous precedent - raising fears that other weaker European nations might pull the same trick.

That would require a much larger recapitalisation process than would be needed to just cover Greece's debts. That could leave EU taxpayers facing a bill of €290bn.

Here's their working out:

The rationale for injecting more capital into banks would presumably be to enable them to cope with a larger write-down on the value of their holdings of Greek government debt than the 21% "haircut" proposed on 21st July as part of Greece's €109bn second bail-out package.

Admittedly, a larger "haircut" would be good news for Greece (if not her banks). But it could set a dangerous precedent that could quickly cause renewed jitters in the markets. This is because investors would presumably worry, more than they are already, that other troubled governments in the euro-zone would try to obtain similarly large "haircuts" on their own debt before too long.

Since the aggregate exposure of the EU banks subjected to the EBA's stress tests in July to the government debt of Ireland, Portugal, Spain and Italy combined was roughly seven times their exposure to the government debt of Greece, large-scale across-the-board haircuts would naturally fuel concerns that the banks could not cope unless they were injected with vastly more capital than required to deal with a default by Greece alone.Indeed, a 50% "haircut" on the banks' exposure in their banking books at that time to the government debt of all five countries would generate a loss of just under €290bn based on the EBA data. Injecting capital on this scale, let alone to deal with the banks' exposure to other troubled assets, would mean a massive transfer of risk from the banking sector to the public sector, magnifying investors' concerns about the sovereign debt crisis.

Over in New York, the stock markets is enjoying a better day. Dominic Rushe has the details:

US stock markets are all up as Wall Streeters decide where to go for lunch. The rally started after some better than expected jobs figures were released by Automatic Data Processing.

The private sector created 91,000 new jobs in September, analysts had been predicting 75,000. Merkel's comments on prospects for efforts to stabilize Europe's banks also seems to have cheered investors.

The Dow Jones Industrial Average is up marginally at the moment. It closed up 1.44% yesterday, the first gain in three trading days.

As Jill Treanor reported earlier, there's been a major shake-up at UBS.

Francois Gouws and Yassine Bouhara, co-heads of Global Equities, have both resigned. And "disciplinary action" is planned for several other UBS staff. Jill's blog has more details.

The International Monetary Fund has urged Europe's leaders to recapitalise their banks quickly - rather than procrastinating any more and letting the crisis get any worse.

Antonio Borges, the IMF's Europe director, said there was a real risk of a new credit crunch unless Europe's weaker banks were bolstered:

We have to restore confidence quickly. The best way to do that is to have a capital increase rather quickly.

Angela Merkel's comments earlier today that a deal could be hammered out by 18 October must have been just what the IMF wanted to hear.

Borges also said that the IMF had no intention of intervening in the bond markets - as it simply doesn't have the authority. Its firepower can only be directed straight at individual countries. This is something of a u-turn on previous suggestions that the Fund could buy bonds to prevent the crisis spreading to Italy and Spain.

The Financial Times is reporting this evening that Europe's banking regulator has been asked to test how a large Greek debt write-down would affect the strength of Europe's banks.

Initial reaction -- About Time Too!

As the FT puts it:

The move, a tacit admission that the European Banking Authority's two previous rounds of bank stress tests were not sufficiently robust, came as Angela Merkel, the German chancellor, said she was prepared to recapitalise her country's banks if necessary.

However, EU officials are insisting that this "was not an indication" that a Greek default was imminent (perish the thought!).

More on the Pink 'Un (registration required).

From Brussels, David Gow reports that Angela Merkel's government are planning a "three-pronged" strategy to bank recapitalisation:

1) Banks raising fresh capital on their own. If they fail then....

2) National governments will stop in and, finally....

3) the bailout fund, the European Financial Stability Facility will become involved.

However, at €440bn, would the EFSF be big enough, on top of its other obligations - including making precautionary loans to eurozone nations, and intervening in the bond markets?

Irish finance minister Michael Noonan indicated this afternoon that around €100 would be needed to recapitalise European banks. As we pointed out earlier, though, Capital Economics reckons it could cost more than €270bn.

While politicians and bank bosses scramble to agree the details of Dexia's rescue package, the Franco-Belgian bank has been savaged today by French mayors.

Several civic leaders told a parliamentary hearing that they had been "tricked" into signing up for loans which left them facing huge interest payments.

As my colleague Kim Willsher reported last month, these loans were typically pegged to the Swiss franc. It has soared in value in recent months as investors sought safety from the crisis - pushing up the repayment costs.

Reuters has more details of today's hearing:

Several mayors have sued Dexia over these so-called "toxic" loans, which they say were presented as "fixed" interest-rate products pegged to exchange rates such as the euro-Swiss franc.

When the new rates kicked in, the local authorities saw their 4-percent borrowing rates shoot up in some cases to 15, even 24 percent, the mayors told the hearing at France's National Assembly.

"Fixed rate, fixed rate, fixed rate - every time the same words," said Xavier Martin-Le Chevalier, mayor of the northwestern town of Tregastel, holding up Dexia's marketing documents. "There was indeed serious trickery."

Dexia's defence is that the local authorities were clearly informed of any risks.

Wall Street is enjoying a late rally, as optimism that Europe will devise a bank rescue package outweighs fears that the global economy is heading for a (cold) bath.

The Dow Jones just hit its highest level for the day - up 141 points at 10,950.89. Just 20 minutes to go till the close....

Wall Street ended in cheery mood, as the various noises out of Europe reassured traders.

The Dow Jones Industrial Average finished 1.2% higher, or 131.24 points to the good, at 10,939.95. Disney Co was the start performer, up 5.5%.

The S&P 500 gained 1.8%, and the Nasdaq rose by 2.3%.

Just getting some flashes on the Reuters terminal about Dexia. Sounds like the rescue deal won't be completed on Thursday....

21:32 05Oct11 RTRS-DEXIA TO HOLD BOARD MEETING ON SATURDAY TO VOTE ON

BREAK-UP PLAN -SOURCES

21:33 05Oct11 RTRS-DEXIA'S BOARD MEETING TO TAKE PLACE IN PARIS - SOURCES

Just time for a bit of Tim Geithner. The Treasury secretary has just told the Washington Ideas Forum that America's economic recovery is threatened by Europe's debt crisis.

Photograph: Saul Loeb/AFP/Getty Images

Photograph: Saul Loeb/AFP/Getty Images

Geithner told his audience that:

Europe matters a lot to us. We don't want to see Europe weakened by a protracted crisis. Europe understands that.Europe is a large part of the global economy, and a severe crisis in Europe would be damaging.

Geithner also warned that EU leaders were moving too slowly.

Hard to argue with that point - but America's leaders were hardly more nimble over this summer's debt ceiling talks.

Late breaking info before we go - Moody's has begun cutting its rating in Italian banks, following the downgrade to Italy's sovereign credit rating yesterday.

Intesa Sanpaolo has just been cut to A2 from Aa3, that's a two-notch downgrade, with a negative outlook too.

Moody's said the cut "reflects both Intesa's direct exposure to the Italian sovereign and its pronounced focus on domestic business, as revenues generated in Italy provide 77% of the group's revenues."

At A2 (the sixth-highest rating on the Moody's scale), Intesa now has the same rating as Italy. As Moody's pointed out "the credit profile of Intesa is closely correlated with the Italian government's credit profile . Given this correlation, it will be unlikely for Intesa to be rated higher than the Italian government."

More here.

Unicredit's rating has also been cut, to A2.

And we're done. Thanks all. See you again tomorrow.