OK, we're shutting the blog down now (as I seem to have been rather distracted since getting back to the office). And events seem to be over.

Personal note - thanks for kind wishes in the comments below (kizbot, IfigEusLannuon, pesaola, buttros, ballymichael, zenonp, barz, Kyza06, anyone i've missed). Hand on heart - it's the readers who make this blog work (as shown today.).

Goodnight!

Out in Greece, some new polling data suggests that the Syriza party is still leading. It was conducted by the Public Issue company, but it's not clear exactly when the polling took place (ie, before, after or during Alexis Tsipras's trips to Paris and Berlin, and the repeated warnings from EU leaders.)

It's also not quite clear how the data has been adjusted for abstentions and don't knows. So given all that, here are the numbers for you to digest as you see fit:

Syriza 30%,

New Democracy 26%,

PASOK 15%,

Democratic Left 7%,

Independent Greeks 7%,

ΚΚΕ 5%,

Golden Dawn 4.5%.

Hopefully we'll have more details about it tomorrow.

(thanks to @irategreek as ever for the info)

UPDATE:

But as our correspondent in Greece Helena Smith points out the poll once again suggests that the "pro-European" centre-right bloc (now cast under New Democracy) is coming up from behind. This would appear to indicate a trend. In an election campaign that is gearing up along the lines of support for the euro vs the drachma with Tsipras, rightly or wrongly, increasingly portrayed/perceived as being in favour of returning to the country's old currency recent polls have shown Syriza keeping its lead but with its margin dropping considerably.

How low can the euro go while the Greek crisis plays out?

The single currency has avoided heavy losses today, down slightly at $1.2576, but several economists are warning that it will head lower in the weeks ahead.

Capital Economics said this afternoon that it is sticking with its forecast that the euro will slide to $1.10 by the end of this year, but feels there's a growing risk it could fall further, faster.

The euro against the US dollar during 2012.

The euro against the US dollar during 2012.

Some people suggest that the euro has maintained its strength because of theories that the eurozone will end up smaller, and stronger. Capital Economics' Jonathan Loynes reckons not, though:

Not only would it be uncharacteristic for currency markets to be quite so forward-looking, but even a limited euro-zone break-up which sees the exit of Greece and one or two other small countries would still have severe adverse economic and financial effects. And there would surely be, for a time at least, fears of a bigger break-up. Accordingly, it seems more likely that the markets have simply not taken break-up risks very seriously.

If so, that indicates the euro could really tumble if a Greek exit should happen or simply look more likely. Indeed, a research note just released by Citi estimates that the euro will fall to the brink of parity with the US dollar at $1.01.

Europe's stock markets have ended the day in cheery mood -- going some way to recovering from Wednesday's big selloff. Here's the closing numbers:

FTSE 100: up 83 points at 5350, + 1.5%

German DAX: up 30 points at 6315, + 0.48%

French CAC: up 34 points at 3038, + 1.16%

Spanish IBEX: up 93 points at 6534, + 1.46%

Italian FTSE MIB: up 146 points at 13107, + 1.13%

So what's going on? Traders reckon that's a bit of bargain hunting (stocks have fallen sharply in the last two months), and also a slightly more relaxed feeling about the eurocrisis (despite nothing being fixed last night). But given the news this morning that the UK recession is worse than expected, and the poor PMI data from Germany and France, the optimism feels a little stretched:

Michael Hewson of CMC Markets explains:

The fact is, given the sell-off in recent days, none of this data was a real surprise given the economic backdrop across Europe, so to have it confirmed wasn't too much of a shock.

Back out in Berlin, Nick Clegg has declared that he has massive sympathy for the German government as it tried to tackle the Eurozone crisis.

Here's Clegg's quotes, via our correspondent at the scene, Kate Connolly:

If I was a politician of this country I understand how difficult arguably impossible it would be to turn to German tax payers and say look you've been extraordinarily generous in the country which is the paymaster of the EU for many many years, and have provided very generous assistance to weaker economies, to structural funds you've reached deep into your pockets recently to fund assistance packages for countries like Greece; you as a country have been through a painful period of adjustment in the early years of Germany's entry into the Eurozone to make the German economy competitive...in that context to turn round to the German tax payer and say 'could you dip back into your pocket and somehow shoulder the burden of the collective debt of the Eurozone.

Of course that's an extraordinarily difficult thing to ask.

Like any good liberal, Clegg also acknowledged the difficulties that politicians in Italy or Greece faced:

Because of mistakes that are not the fault of the citizens...that those people are now being asked to suffer a steady decline in their living standards that might stretch for years into the future.

Clegg warned that the Euro lacked the mechanisms to deal with shifting resources where they were needed - effectively arguing for full-scale fiscal transfers (which would bring us much closer to a United States of Europe). He said:

If you don't have some mechanism by which you soften the shock for the uncompetitive economies of Europe...some way of either sharing debt or transferring money from strong parts to the weak parts or getting the ECB to be a more active lender of last resort, the only alternative is to ask millions of people to suffer huge declines in their livelihoods over many many years.

Finally, the deputy prime minister argued that stabilising the profound imbalances within the single currency was central to solving the crisis, else society across Europe could deteriorate.

In my view any sustainable solution to the Eurozone has to reconcile those things. IF you only do discipline and austerity what we will see is an increase of real resentment, extremism, xenophobia...and that will not be good for the Eurozone or the European Union as a whole.

Afternoon all (writes a somewhat dazed Graeme Wearden). To business! We have a bit more detail of Mario Monti's suggestion this afternoon that eurobonds may soon be a reality (as Jo flagged up earlier).

Monti was speaking in Rome, where he made a public show of support for collective borrowing – after Angela Merkel rebuffed François Hollande's proposals in Berlin. He said:

Italy is very much in favour of the creation of euro bonds when the time is right,

and we do not expect it to be too far off.

Clearly the issue of eurobonds is going to fester - only a few hours ago, German foreign minister Guide Westerwelle was insisting that Berlin will not cave in (see 1.04pm)

And we've got a bit more detail on Graeme Wearden's win, which I better post quickly before he wrests back control of the blog. The Wincott Foundation said:

Online's ability to bring together text, pictures, graphics, sound and video offers a rich palette for delivering news. From the sharp summons of the tweet to the complexities of journalism based upon analysing and visualizing large quantities of data, online financial journalism is a force to be reckoned with. The judges admired the work of Reuters and the Telegraph in this arena, but felt that this was the year in which to recognize the Guardian, whose commitment to multi-platform on-line journalism is making an impact in stories which range from phone-hacking and last summer's riots to coverage of financial news.

In particular, we liked the Guardian's live blog of Eurozone summits, a format which offers the user instant access to everything from the summit communiqué and gossip to a diverse range of international commentary. It is for this work that we name Graeme Wearden, Business Reporter of The Guardian this year's Wincott Online Financial Journalist.

In the light of the controversial decision recently to award the German company Siemens the British electric trains contract ahead of British companies and at the cost of hundreds of British jobs, Kate Connolly asked deputy prime minister Nick Clegg what advice he'd give to British companies trying to compete for such contracts in future, and what help the government was giving them. She writes:

He responded that the last government had awarded the contract and that it was understandably controversial. "It caused a great deal of controversy, although I don't think it should detract from Siemens' achievement in winning the contract or from the very very significant employment that Siemens generates in the UK and the fact that it's part of the fabric of British life." He added that Siemens had also announced today an increase in the number of apprenticeships it was offering in the UK.

He said the issue was part of a wider topic: "It's an issue about how do we make sure when the government issues public tenders and contracts it does it in a transparent open way where everyone has a fair crack of the whip including companies that are based in or operate in the United Kingdom." He said that business secretary Vince Cable had been very active in working on the issue. "We've looked at and learnt lessons from that contract to make sure that we proceed in a way that gives everyone a fair crack of the whip".

More from Kate Connolly over in Berlin on deputy prime minister Nick Clegg's speech.

To a question as to whether Britain was standing in the way of eurozone progress by 'vetoeing' the treaty at the December summit and whether Britain shouldn't therefore consider becoming instead an associate member of the EU, Clegg said:

"The United Kingdom did not veto the fiscal compact last December, we are just not a part of it... it has taken shape, and I'm very much at one with the German government following discussions (with German ministers) this morning that it is very important that that fiscal compact which is part of the ingredient of a successful Eurozone should be properly respected.

"My own view is that the only way that the eurozone can be restored to full health is through some further changes in rules which govern the Eurozone. Of course we should not, as a non-Eurozone member stand in the way of that. We have a huge strategic self interest in the UK to do everything we can to be cooperative to ensure that the Eurozone is successful."

But he said negotiating a new treaty, unless it was absolutely necessary for the good of the Eurozone, would be counterproductive. At the same time he insisted that if such a decision was taken, "any rational British government, certainly the government that I'm a member of, would not stand in the way of that because it would be cutting off our nose to spite our face".

And congratulations to my colleague @graemewearden who just won the Wincott Award for online business journalist of the year!

Italian prime minister Mario Monti says it will "not be too long" before euro bonds become reality.

Nick Clegg listens to German Foreign Minister Guido Westerwelle, unseen, during a news conference after a meeting at the foreign ministry in Berlin earlier today. (AP Photo/Markus Schreiber) Photograph: Markus Schreiber/AP

Nick Clegg listens to German Foreign Minister Guido Westerwelle, unseen, during a news conference after a meeting at the foreign ministry in Berlin earlier today. (AP Photo/Markus Schreiber) Photograph: Markus Schreiber/AP

More from our Berlin correspondent Kate Connolly, who was watching Nick Clegg speak at the British embassy in Germany earlier today. (See 2.54pm)

Clegg heaped praise on Germany saying at a time when Britain was needing to "rewire" itself and restructure its economy, Europe's economic powerhouse held a lot of lessons from which Britain could learn.

"It is immensely important in the United Kingddom that we learn constantly from the outstanding example of the way in which Germany is an economy built on investment, not debt, on investment and research, not squandering resources today on the never-never, and constantly striving to be the exporting powerhouse that Germany indeed is.

"Because the United Kingdom's economy has been very unbalanced in the last 10, 20 years as we've become over reliant on one sector: financial services, and in one part of the country. So celebrating manufacturing, celebrating engineering, is absolutely essential to our rewiring, to our reinvention of the British economy."

The Danish central bank has just cut its key interest rate from 0.7% to 0.6%.

The Danish crown has risen to a five-month high against the euro as investors flock to the currency for protection against a euro break-up. As Reuters explains:

Investors are betting that if the euro broke apart, Denmark would peg the crown to Germany's currency, whether the euro or a successor, as Germany is Denmark's biggest trading partner. Buying crowns is seen as a way of gaining exposure to Germany without the risks associated with holding euros.

The rise in the Danish crown led to talk that the central bank might raise interest rates, but it seems to be going in the opposite direction.

Back to Germany, where our Berlin correspondent Kate Connolly has more detail from Nick Clegg's speech at the German launch of the Queen Elizabeth Prize for Engineering.

Deputy prime minister Nick Clegg stressed that the Eurozone's problems were Britain's problems, and that a "successful Eurozone is absolutely indispensable to a successful British economy." He added: "Three and a half million people depend for their jobs in the UK on our presence in an integrated single market in the European Union... we cannot grow if the Eurozone doesn't grow."

He said as a result Britain wanted to see the problems of the Eurozone tackled as fast as possible. "We want to play our part even though we're not members of the Eurozone in this wider discussion which must come to a comprehensive solution fast."

The election in Greece, he said, came at a very important moment in the Eurozone drama. "No-one should think in any way that Greece leaving the Eurozone is in any way a cost-free option. The knock-on effects are entirely unpredictable and could be calamitous, not only for other members of the Eurozone but for the European Union as a whole and would affect directly the United Kingdom economy as well.

"We've mustered the political will to solve these crises in the past, we can do it again. And it's not just our economy that is at stake if we don't rise to the occasion...it's our politics as well. Because if there's one thing we know from our own shared history is that a combination of intense economic and social insecurity and widespread public disillusionment with governments and political leaders which exists now across the European continent, is the ideal recipe for political extremists, chauvinism and xenophobia."

The euro has just spiked to its highest level versus the Swiss franc since mid-March. There were immediate questions over whether it was a sign of intervention by the Swiss but those seem to have been quashed.

Steve Collins, global head of dealing at London & Capital Asset Management, suggests it was the result of a non-European investor buying aggressively following the rumour that the Swiss government might impose a tax on Swiss franc-denominated deposits. Several others then tried to buy and in Collins's words "we had a nice squeeze". There are also rumours that it was a fat finger trade.

David Bloom of HSBC explains why the market is currently so jumpy where it comes to the Swiss franc.

It's an unsustainable situation. [The Swiss] have won the battle but they will ultimately lose the war. They have won the battle against a rapidly appreciating currency, but when you have serial devaluers like the US and the UK, if you run good public finances and you have massive assets, you're going to be a strong currency whether you like it or not. You can see why the market is so nervous. They believe the Swiss have an unsustainable policy that will need more and more firepower.

I'm all right Jack. Sweden says it is "well prepared" for any Greek eurozone exit, according to Reuters, citing Sweden's financial markets minister.

Growth in US manufacturing slowed in May, according to a new industry survey. Markit's new flash PMI for the US dropped from 56 to 53.9. A reading above 50 shows the sector continued to grow, although at a slower pace. Markit economist Chris Williamson said:

US manufacturing seems to be repeating the trend seen in the previous two years, whereby a strong start to the year loses momentum as summer approaches. This year, the cause seems to lie largely with weak export sales, which likely reflects the deteriorating economic situation in Europe as well as slower growth in China.

Over in Berlin, our deputy prime minister Nick Clegg is speaking at the British Embassy.

Now the DPM is wowing the crowd in the British Embassy with his fluent German. twitter.com/jessbrammar/st…

— Jess Brammar (@jessbrammar) May 24, 2012

He said no-one should think Greece leaving the eurozone was in any way cost-free. The knock-on is entirely unpredictable and could be calamitous and it will affect UK economy.

He also explained his position on the financial transaction tax, saying he would support it if he thought it would boost growth, but an EC study said it would, in fact, cost 500,000 jobs. The deputy prime minister also reacted to today's miserable GDP figures.

The revision is very disappointing ... We are shifting up a gear in our zeal to see the economy grow.

German Chancellor Angela Merkel has said that budget consolidation and pursuing economic growth are two sides of the same coin.

Speaking at an event for the German electrical industry, she reiterated her opposition to eurobonds. But she recognised that Germany must help other eurozone members if it wants to help itself.

At the moment we're not quite free of (our) worries... We'll only be in good shape if our neighbours are also doing alright.

Germany's standing firm on its rejection of eurobonds, according to ITV News economics editor, Richard Edgar.

Ger foreign minister Westerwelle tells me "we can't solve a debt crisis by taking up new debts" - no softening on Eurobonds

— Richard Edgar (@ITVRichard) May 24, 2012

For anyone wanting to know more about eurobonds, my colleague Phillip Inman has created an essential guide.

Following today's PMI data from the eurozone countries, there's some great analysis from FT Alphaville (behind the paywall) on the usefulness (or otherwise) of the aggregate eurozone PMI data.

The suggestion is that big countries like Germany and France are assigned such big weightings for the aggregate figure that the smaller countries barely have an impact. The aggregate picture is therefore largely unaffected by the miserable economic situation in peripherial countries.

Greece is not enjoying the rally seen in markets across Europe. The Athens Stock Exchange is now down 3.42%, with the banks down 3.86%. (Thanks to Greek journalist @EfiEfthimiou)

The lower house of the Dutch parliament has approved the eurozone's permanent bailout fund, the European Stability Mechanism. The upper house, or Dutch Senate, still needs to approve it. The ESM can lend up to €500bn to bail out members of the eurozone.

Geert Wilders, leader of PVV. Photograph: NOS news

Geert Wilders, leader of PVV. Photograph: NOS news

Far-right Dutch politician Geert Wilders filed a lawsuit earlier this week aimed at postponing ratification of the ESM until after elections on September 12, but he is not expected to succeed. (Story in the FT, behind the paywall).

The FTSE 100 has rallied over the day, recovering from yesterday's sharp losses. It may be a case of, the news is so bad it's good, as traders hope for more quantitative easing after the revised GDP figures showed the UK was in a deeper recession than previously thought (see 9.31 onwards).

FTSE 100: up 1.4%

France CAC: up 1.4%

Germany DAX: up 0.8%

Spain IBEX: up 1.4%

Italy FTSE MIB: up 0.5%

Regular reader, and commentator, Theodora Oikonomidis has translated last night's statement from EU leaders on the Greek elections into plain English:

Whoever you vote for, we want them do what we tell them anyway.

Which is a good a moment as any to hand this over to my colleague Jo Moulds for a while...

Italy's deputy finance minister clearly didn't hear Angela Merkel's concerns about people discussing Greece's possible exit from the euro (see 11.12am)

From Reuters in Rome:

Italy must prepare itself for the possibility that Greece may leave the euro zone, but the aim is to avoid that option, Italy's Deputy Economy Minister Vittorio Grilli said on Thursday.

He spoke on the sidelines of a business lobby conference in the capital.

European Central Bank policymaker Ewald Nowotny was in bleaker mood in Vienna today, saying a Grexit would create "large, massive shocks where you would not know what the consequences would be".

Britain's deputy prime minister is in Berlin today to launch a strongly worded attack on Europe for its response to the crisis that has shaken the currency union to its core.

Nick Clegg will say the EU's response has been woefully fragmented and damaging to public confidence. Our political editor, Patrick Wintour, says the speech will outline how the Liberal Democrat party's approach to the crisis differs from David Cameron's Conservatives. The former MEP is expected to warn that:

We have created different classes of country: strong and weak, spenders and savers, eurozone and non-eurozone. But these divisions are false. Europe's economies cannot be prised apart and filed neatly in different boxes; they are too interdependent.

And we the way we take decisions is undermining public confidence. Every few weeks European leaders sit down to yet another crisis summit, where another temporary solution is agreed. The tree is falling, and we are pruning one leaf at a time. It is piecemeal politics; endless tactics with no strategy.

More here, and full details later.

The former European Commissioner will also attack the idea that a Greek euroexit could be handled, as:

Greece's caretaker prime minister Panagiotis Pikramenos has spoken about last night's summit, focusing on the desire of EU leaders for Greece to remain in the 17-nation euro bloc.

Helena Smith reports:

Addressing Greeks after the summit, the high court judge said EU leaders had expressed their "strong desire" for the debt-stricken country to remain in the single currency as long as Athens "fulfilled its obligations" in the form of ongoing austerity and corrective reforms.

The interim PM said he had impressed the need for "immediate action" to be taken to stimulate growth, going so far as to call for the European Investment Bank and EU structural funds to "lead the way" in kick-starting Greece's cash-starved economy. And there was another thing Greeks should know:

During their pre-summit meeting, Angela Merkel had voiced "deep dissatisfaction" over reports that Greece was heading for the euro exit door, he said. Clearly the Germany chancellor is not on the same page as her Bundesbank.

As regular readers know, yesterday the Bundesbank said that a Greek euro exit would be manageable, and on balance a better option than allowing the country to renege on its obligations.

German and UK sovereign debt has strengthened to record levels in the face of bad econonic news from Britain (the deeper recession) and Germany (a shrinking private sector).

This drove down the yield on UK 10-year gilts to a new all-time low of just 1.739%, while German 10-year bunds were changing hands at a record low yield of just 1.375%.

It sounds like good news for both countries, as it shows they can borrow at cheaper rates than ever before. But economists fear that the low yields, particularly for Germany, are a sign that the financial system is breaking down. Investors, fearing that the financial crisis is about to flare up again, are trying to preserve their capital by finding a safe home for it, regardless of the low rate of return.

Of course, the unconventional monetary policy operated by the Bank of England (£325bn of quantitative easing) and the ECB (€1trn of cheap three-year loans), are also affecting the bond markets – meaning there is much more money swilling around.

Photograph: Orestis Panagiotou/EPA

Photograph: Orestis Panagiotou/EPA

News in from Greece where Helena Smith our correspondent says reaction to the summit has been lukewarm.

The Greek media this morning are also highlighting the growing chasm between Germany and France over eurobonds (as Ian Traynor reported last night). The talk is about how Europe's debt crisis is turning into a banking crisis and political crisis too.

Helena reports that radio channels are highlighting the second sentence of the statement released by EU leaders: "We are fully aware of the significant efforts already made by the Greek citizens."

At this stage of the crisis – now into its third year – with a good deal of the Greek population pauperised by biting austerity measures enforced at the behest of the EU and IMF in return for rescue loans, some commentators said it was long over-due concession.

But primarily the EU summit was seen, once again, as an attempt to kick the can down the road – this time to the Greek elections on June 17.

"The European Union will vote after Greece," opined the left-leaning Ta Nea. "Decisions were delayed until after the elections but the message to Athens was "keep your promises to stay in the euro."

It was not lost on the media that the first attempts at changing the fiscal recipe were made as leaders chin-wagged over the informal dinner in Brussels. But it was also noted that such efforts were not without their own friction. "The knives came out over dinner," noted the mass-selling To Ethnos. "The frontal collision between Hollande and Merkel over growth and eurobonds marked the dinner of EU leaders in Brussels. Accounts were left open until the next summit."

Several analysts are pointing out that although the UK economy shrank by 0.3% in the first three months of 2012, government spending increased by 1.6% compared with a year ago. That doesn't indicate that austerity-driven spending cuts alone has directly driven the UK economy into a contraction (although the fall in construction output has been blamed partly on a drop in large public sector contracts, and consumer spending has clearly been suffering too).

UPDATE: Our full story on the UK GDP data is now live, here

Economists are disappointed by the news that the UK economy shrank by 0.3% in the first quarter of this year, which confirms Britain's double-dip recession (see 9.31am onwards)

Howard Archer of IHS Global Insight said the UK economy was undeniably struggling. He expects GDP to start rising later in this year, but warned:

hopes of modest sustainable recovery developing during the second half of the year could be scuppered by events in Greece.

Simon Hayes of Barclays Capital said that the drop in GDP was partly due to a fall in stock building by businesses. That shows "firms becoming very cautious about the outlook for demand, so are running down their stocks".

That's looks like another sign that UK companies are hunkering down in the face of the eurozone crisis.

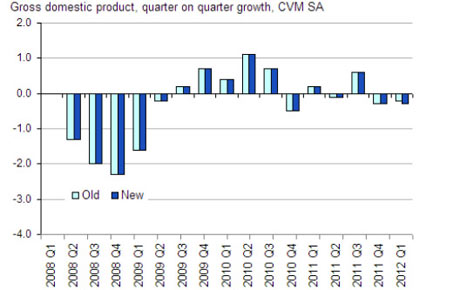

This graph from the ONS shows how the UK economy has struggled to post strong growth over since the financial crisis began:

Light blue is the first estimate, dark blue for revisions.

You can also see all the data, back to 1948, on our datablog.

Here's the break-down of the new UK GDP data:

Production sector output: -0.4% (with manufacturing flat)

Service sector output: +0.1%

Construction sector output: - 4.8%

This morning's downward revision to UK GDP also means that the UK economy is actually slightly smaller than 12 months ago. On a year-on-year basis, UK Q1 GDP was 0.1% lower than the first three months of 2012 (down from a previous reading of flat).

The ONS attributed this to:

Global economic headwinds as well as domestic economic conditions such as the impact of continuing high rates of inflation in the UK.

This is mirrored in the labour market where employment has been fairly static.

The Office for National Statistics explained that it has revised down UK GDP (see 9.31am) due to weak construction output.

The -0.3% contraction means that the UK economy shank as much as Spain in the first three months of 2012. The downward revision means the UK's double-dip recession is deeper than feared, and is an even starker contrast with Germany (which grew by 0.5%).

Breaking news - the UK recession is worse than thought. The Office for National Statistics just reported that British GDP shrank by 0.3% in the first three months of 2012, not the 0.2% contraction first reported.

More to follow.

Photograph: Francois Lenoir/Reuters

Photograph: Francois Lenoir/Reuters

David Cameron spoke bluntly to reporters after the Brussels summit concluded last night, hitting out at proposals for a financial transaction tax (FTT) (or Robin Hood tax).

Sky News has the quotes:

Leaving the summit in the early hours, Mr Cameron said: "There were good innovative ideas that can help growth in Europe, but frankly there were some bad ideas too.

"A financial transactions tax is a bad idea, it will put up the cost of people's insurance, put up the cost of people's pensions, it would cost many many jobs, and it would make Europe less competitive and I'll fight it all the way.

That may disappoint, but probably not surprise, campaigns for a FTT, such as Oxfam, which argues that it would "boost growth and protect our economy from future shocks as well as raising money to help those hit by a crisis they did nothing to cause."

City analysts are united in giving last night's summit a resounding shrug.

Here's a round-up of early comments (reminder: the official statement is here):

Gary Jenkins of Swordfish Research

Well for once a European summit did not disappoint; they promised nothing and that is exactly what we got...

It would appear that Greece will need further debt forgiveness and unless the EU is prepared to agree to that then a messy divorce could be on the cards in the future.

Nicholas Spiro of Spiro Sovereign Strategy.

Fears over the fallout from Greece's possible exit from the eurozone are being fanned by growing Franco-German splits over crisis management.

It's one thing to disagree about shoring up Europe's banks and bond markets in a period of relative calm, but quite another when contagion is back with a vengeance.

Investors should be singing the praises of President Hollande since he is leading the push for a speedier move towards fiscal integration. In our view this explains why the markets have a rather nuanced view of France's new government. When it comes to stemming contagion, France is on the side of the markets.

Elisabeth Afseth of Investec

The European leaders want 'Greece to remain in the Euro while respecting its commitments' – there's a surprise....

There appear to be less threats of a Euro exit coming, this may just be a coordinated effort to avoid disrupting markets, or it could be indicative of a more genuine fear of what an exit would look like and of the effort that is likely to be made to keep Greece in.

Sony Kapoor of Re-Define

History will not be kind to the current crop of European leaders There are no heroes! Massive avoidable social & economic costs [lie ahead]

Chris Weston of IG

The EU Summit came and went without incident, with all the key players getting their points across....It does feel that something big is bubbling away in the background that will change the course of Europe forever; perhaps we will know more in a month, perhaps six months or even a year. However, it does feel that something is going to need to happen to install a huge amount of confidence, or it will be lost in a massive way.

Michael Hewson of CMC Markets

Last night's decision by EU leaders to put off any proposed action until next month's June summit with respect to dealing with the problems afflicting Europe's banking sector, illustrates the paralysis at the heart of Europe's policy making machinery, and also the divisions as to what any next steps would be to restore investors fragile confidence.

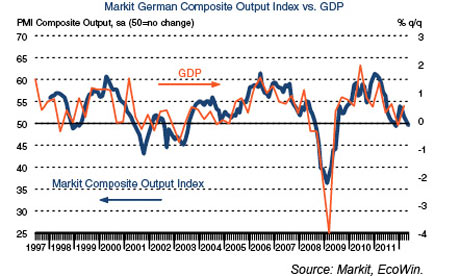

More bad economic news – economic activity in Germany's private sector fell last month, with manufacturing shrinking at its fastest pace in three years.

Hot on the heels of the poor results from France, Markit announced that the German 'composite PMI' (which tracks services and manufacturing output) fell to 49.6 (from 50.5). That's a six-month low, and below the 50-point mark which separates expansion from contraction.

Markit reported that this is the first time that Germany's private sector has shrunk since last November - another sign that the eurozone economy is may be weakening.

It's not all bad news for Europe's powerhouse, though. Earlier data confirmed that it grew by 0.5% in the first three months of 2012.

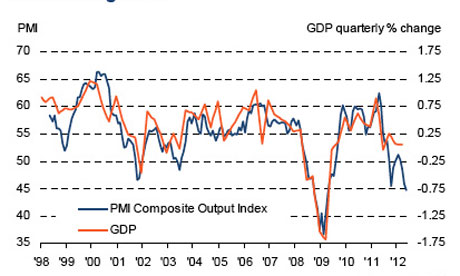

Worrying economic news from France, where activity in its private sector has fallen to a three-year low. This suggests the French economy is contracting – bad news for new president Hollande.

Data firm Markit just reported that the composite measure of French services and manufacturing output fell to 44.7 in May, from 45.9. That means activity shrank, to its lowest level in three years.

This graph shows how the PMI (based on interviews with purchasing managers), is a pretty good leading indicator of GDP. Any PMI reading below 50 shows that activity contracted. The French economy was stagnant in the first three months of 2012.

Markit's Jack Kennedy said:

The PMI data points firmly towards a contraction in second-quarter GDP following stagnation in Q1.

Europe's financial markets have opened higher this morning, despite the lack of progress in Brussels overnight. The main indices are up between 0.7% and 1%, with the FTSE 100 gaining 40 points to 5307.

This only claws back a small slice of yesterday's panicky selloff, which saw £35bn wiped off the FTSE 100 during a 136 point tumble.

From Brussels, our Europe editor Ian Traynor reported in the early hours of the morning that a "major rift has opened up between Germany and France" over how to restore confidence in the euro, for the first time since the crisis began.

Ian confirms that France's president François Hollande challenged Germany's chancellor, Angela Merkel, insisting that collective borrowing needed to be put on the table as an option for saving the currency. He writes:

Hollande told the dinner of 27 leaders that he wanted to see eurobonds established, while conceding that this would take time, witnesses at the talks said.

Merkel responded that this was nigh-on impossible since it would require changes to the German constitution and around 10 separate legal changes, the sources said.

There was no policy breakthrough at the summit, rather a reiteration by leaders of known positions. Any decisions were postponed until the end of next month after French and Greek parliamentary elections on 17 June.

The Daily Telegraph's Bruno Waterfield was also in Brussels, and wasn't too impressed by the new French president's performance:

#eurozone: #Hollande, the charisma of Van Rompuy, the razor like clarity of Barroso and the prose of a euro communique twitter.com/BrunoBrussels/…

— Bruno Waterfield (@BrunoBrussels) May 23, 2012

Here's the official statement released by the EU leaders in the early hours of this morning, after last night's informal summit.

We discussed the political and economic situation in Greece. We want Greece to remain in the euro area while respecting its commitments. We are fully aware of the significant efforts already made by the Greek citizens.

The euro zone has shown considerable solidarity, having already disbursed together with the IMF nearly €150bn euros in support of Greece since 2010. We will ensure that European structural funds and instruments are mobilised to bring Greece on a path towards growth and job creation. Continuing the vital reforms to restore debt sustainability, foster private investment and reinforce its institutions is the best guarantee for a more prosperous future in the euro area.

We expect that after the elections, the new Greek Government will make that choice.

Good morning, and welcome to our rolling coverage of the eurozone debt crisis.

A few hours ago, the informal EU summit in Brussels ended after discussions which showed Europe remains deeply divided over the way through the crisis.

Speaking after the talks, sources told our Europe editor Ian Traynor that the rift between France and Germany widened, over the troublesome issue of collective borrowing.

We'll be tracking all the reaction to the events in Brussels over the next few hours.

Also coming up ... it's a busy day for economic data, with the second estimate of UK GDP for the first three months of 2012 being released. Will Britain's double-dip recession be confirmed? New surveys of Europe's manufacturing and service sectors will also show how the region's economy fared this month.

Here's an early agenda:

• French manufacturing/services PMI for May: 8am BST / 9am CEST

• German manufacturing/services PMI for May: 8.30am BST / 9.30am CEST

• German IFO business confidence survey: 9am BST / 10am CEST

• UK GDP for Q1 2012, first revision: 9.30am BST