And with that its time to close up on another busy day, with a new president for Greece and a date for new elections.

David Cameron and Mervyn King voiced their concerns about the eurozone crisis, and there was confusion over whether the ECB had stopped supporting a number of Greek banks (it seems it hasn't).

We'll be back tomorrow for more on Greece, Spanish GDP and US weekly jobs claims. Until then, thanks for all the comments and have a good evening.

There is a good explanation of what's been happening with the ECB and the Greek banks on FT Alphaville.

Essentially, the Greek banks are using the emergency liquidity assistance until the EFSF agrees to release its bonds, so they can use these as collateral. The delay seems to be just a technicality. Alphaville says:

The really important point to end on is that as soon as the EFSF bonds are transferred over (hopefully Wednesday's misconstrued mess will focus a few bureaucratic minds), these Greek banks can go back to pledging the EFSF collateral at normal ECB ops. The brief spell in ELA ends. Incidentally, these brief switches in and out of ELA have also taken place in Irish banks and in Dexia when collateral requirements shifted against banks a few times, only to shift back later. World didn't end then.

Greece's new prime minister, Panaghiotis Pikrammenos, is due to be sworn in at 8pm local time, 6pm GMT.

Here's a profile of the man from Helena Smithin Athens:

Greece's new prime minister Panaghiotis Pikrammenos is president of the country's top administrative court, the council of state. A specialist in Greek constitutional law, the high court judge was seen as a safe pair of hands at the helm of a government that has a lifespan of less than five weeks. "It is a purely caretaker administration that will act within the framework of the constitution," said the French-trained legal expert in his first public statement.

Born in Athens in 1945 as Greece was poised to descend into brutal civil war, Pikrammenos is part of the country's old bourgeoisie and has been described as "decent and well-mannered."

"He is very good at deflecting tensions and keeping the peace," said one insider. "At the high court he has shown some agility in being able to manoeuvre and keep the right balances. They are assets that may well be useful."

The gray-haired judge said he had read about his appointment in the papers and joked he had been chosen because of his surname which means "bitter" in Greek.

"I read that because of my name I was the most suitable person to become the last prime minister of the metapoliteusi [the period following the restoration of democracy with the collapse of military rule in 1974].

"I hope that after me a period of regeneration will begin for our beautiful country."

European markets are closed, and a promising rally after better than expected US figures has been nipped in the bud.

The latest bit of negative news is the ECB stopping monetary policy operations with some Greek banks, putting more pressure on the country's financial position.

So the FTSE has finished 32.37 points lower at 5405.25, Germany's Dax is down 0.21% and Spain's Ibex is down 1.33%. France's Cac managed to edge up 0.34% however.

On Wall Street the Dow Jones Industrial Average is up 25 points at the moment, but is well off its earlier highs.

But the Athens market has lost 1.33%, with the banking index down 7%, not surprising given all the uncertainty surrounding the sector.

More on the ECB and the Greek banks, from Reuters:

The European Central Bank has stopped monetary policy operations with some Greek banks as they have not been successfully recapitalised, euro zone central bank sources said on Wednesday.

The ECB declined to comment.

The ECB only conducts its refinancing operations with solvent banks. With no access to ECB funds, the banks concerned must go to the Bank of Greece for emergency liquidity assistance (ELA).

It was unclear exactly how many banks were affected.

One person familiar with the matter said four Greek banks' capital was so depleted they were operating with negative equity capital. According to its own rules, the ECB cannot provide liquidity to banks in such a situation.

The ECB said earlier on Wednesday it continued to support Greek banks.

Speaking of the ECB, markets are coming under pressure again after this:

ECB STOPS MONETARY POLICY OPERATIONS TO SOME GREEK BANKS AS RECAPITALISATION NOT IN PLACE -CENBANK SOURCE

— Steve Collins (@TradeDesk_Steve) May 16, 2012

Earlier we reported that EU had given its blessing to the release of €18bn in recapitalization funds for Greeks banks. (9.30 am)

Mario Draghi, the president of the European Central Bank, has said his strong preference is for Greece to remain in the eurozone, although it is not for the central bank to decided.

But he seemed to come close to accepting a Grexit could happen, saying the bank would not compromise its principles on price stability to prevent it happening. Bloomberg has this report.

Angela Merkel, by the way, has announced a replacement for her environment minister after he led her conservatives to a defeat in the weekend's state elections. Norbert Roettgen is giving way to Peter Altmaier, the conservative leader in the Bundestag.

Here's more on David Cameron's comments earlier on a possible break-up of the eurozone. My colleague Patrick Wintour writes:

Cameron appeared to cast doubt on the future of the euro during prime minister's questions when he said the eurozone "either has to make up or it is looking at a potential breakup".

He told MPs: "That's the choice they have to make and it is a choice they can't long put off." His aides said later he had not made a mistake with his remarks, which Labour immediately pounced on, accusing the prime minister of stoking fears of a breakup.

The full story is here.

Ahead of Merkel's statement, German finance minister Wolfgang Schaeuble has been banging the drum for even closer European integration.

He has said the European Union's executive commission should become a government for the region, with an elected European president. Schaeuble is one of the most pro-European ministers in Merkel's coalition, but can you imagine the opposition to such an idea?

Meanwhile, after the recent market gloom, some better than expected US housing starts and industrial production figures have given investors a lift.

In early trading on Wall Street, the Dow Jones Industrial Average is up more than 70 points and the FTSE 100 is trying hard to stagger into positive territory. The French and German markets have edged higher but a bit of upbeat US data is not enough for Spain, down 0.24% or Greece, with the Athens market 1.6% lower.

We should hear more from Angela Merkel shortly - there are reports the German Chancellor will issue a statement at 3.30, in other words in around half an hour's time. (There's a live stream in German expected here.)

Paul Mason, Newnight's economics editor, has written a fine blog post about how the deposit flight from Greek banks, and possibly those in other countries too, could be the blow that cracks the eurozone.

The key is the system, called Target 2, that allows euro banks to transfer money within the single currency region, via their central banks. That system is based on banks creating liabilities within the system, secured against collateral:

The Bank of Greece has permission from the ECB to lend against poor collateral up to a certain amount, set twice a week. If that amount is breached, the ECB must vote to raise it: that vote will be effectively a vote to allow massive capital flight.

Should that limit not be raised, Greek banks would be unable to operate...

leading to capital controls, and losses for account holders when the inevitable euro exit occured. More here.

And as Daniel Furr warns on the Huffington Post today, that would put the fabric of the European Union under great pressure:

The euro crisis has viscously exposed the forgotten tensions and fragility, which encouraged the rearming of national economies. Deficit reduction plans have become a race to the bottom with nations undermining each other to ensure their economy is the most productive and competitive post-crisis. It is difficult to even consider the Fiscal Treaty ever becoming a reality after several European governments have used it as a political football.

And that's a good moment to hand over to my colleague Nick Fletcher....

Here's a picture of Greece's new interim prime minister:

Photograph: Eurokinissi/AFP/Getty Images

Photograph: Eurokinissi/AFP/Getty Images

Taken last December, it shows Panagiotis Pikrammenos in his usual role as a president of the Greek Council of State.

The head of the body representing Greece's creditors has warned this lunchtime that Europe's crisis firewall is not large or flexible enough to handle the crisis.

Charles Dallara (who represented bondholders in the recent debt swap) said it would be a "welcome" move if Europe's rescue funds were allowed to invest directly in Spain's troubled banks (something the IMF also recently called for).

Dallara, who runs the International Institute of Finance, also said that Greece's banking system would collapse if it quit the euro, but said a Greek exit was "far from inevitable".

Angela Merkel has managed to calm the financial markets today, by indicating that she might offer Greece more help to remain in the eurozone.

The German chancellor told CNBC that it would be "good for Greece, and for all of us" for the country to stay in the euro, adding:

If Greece believes that we can find more stimulus in Europe in addition to the Memorandum* then we have to talk about that.

* - the austerity measures agreed with the Troika.

Hearing these words, traders were optimistic that François Hollande had an effect on Merkel, at their meeting last night.

Merkel's spokesman Steffen Seibert then reiterated this point, telling a news conference that the German government was prepared to listen to new ideas to stimulate the Greek economy.

Seibert said:

We want to stabilise Greece within the euro. That has been the goal of our policies from the start...

Where there are opportunities for additional growth impulses in Greece, via

support for Greece's own efforts, we are open to listen to such proposals or make proposals of our own.

So, perhaps a softening from Berlin? The result is that the UK and German markets are now almost flat, while the French CAC is up by 1%.

The choice of Panagiotis Pikrammenos as Greece's interim prime minister (see 12.08pm) is not without controversy. Helena Smith has more:

It emerges that the leaders of Pasok and New Democracy - what are now widely referred to as the two "pro-European centrist" parties -- wanted the technocrat banker, Lucas Papademos, to stay on in the post. Regular readers will recall, however, that Papademos who has headed the country's interim left-right coalition government for the past six months, had made clear he was keen NOT to stay on.

With a crucial upcoming NATO summit and EU leaders also re-convening to discuss the issue of re-energising growth and development, both Pasok leader Evangelos Venizelos and New Democracy's Antonis Samaras were keen to have a safe pair of hands in the post. Emerging from the meeting Panos Kammenos, who heads the stridently anti-austerity Independent Greeks party emphasised the "caretaker" role of the new administration. "It will not be able to pass any laws," he told reporters.

The new PM's surname is also written as 'Pikramenos' which, Greek experts such as @Finisterre67 inform me, means 'bitter' in the sense of 'grieved' in Greek. Appropriate, somehow...

Photos from today's meeting of Greek political just landed:

Photograph: Pantelis Saitas/EPA

Photograph: Pantelis Saitas/EPA

What an unhappy bunch they look (and no wonder). From left to right, we have Aleka Papariga of the Communist party; PASOK leader Evangelos Venizelos; , New Democracy's Antonis Samaras; Greek President Karolos Papoulias in the centre; then Coalition of the Radical Left (SYRIZA) leader Alexis Tsipras; Panos Kammenos of Independent Greeks; and Democratic Left leader Fotis Kouvelis.

David Cameron urged European leaders to get to grips with the crisis, telling MPs at Prime Minister's Questions this lunchtime that the eurozone has got to:

Make up, or break up.

Britain's position remains that the inevitable logic of monetary union is closer fiscal union, according to this morning's lobby briefing in Westminster.

Breaking news from Greece -- the meeting of party leaders at the presidential palace has ended (Helena Smith reports)

NET TV is reporting that the election will be held on June 17 with supreme court judge Panagiotis Pikrammenos heading the caretaker administration .

Pikrammenos was seen as the front-runner yesterday.

Photograph: David Levene for the Observer

Photograph: David Levene for the Observer

Financial markets have recovered some of this morning's big losses, but shares are still down sharply in the City. Here's a round-up:

FTSE 100: down 52 points at 5385, -0.97%

DAX: down 50 points at 6350, -0.79%

CAC: up 12 points at 3051, +0.4%

IBEX: down 48 points at 6653, -0.7%

FTSE MIB: down 32 points at 12279, -0.24%

Spanish 10-year bond yield: 6.3%

Italian 10-year bond yield: 5.98%

The euro is trading around $1.271 against the US dollar, and 79.8p against the pound.

Greece's outgoing finance minister Filippos Sachinidis has been in unusually outspoken form this morning, ahead of the meeting of all-party leaders to pick an interim prime minister.

With the meeting effectively passing the baton onto a new caretaker government, Sachinidis has taken the opportunity to speak bluntly. From Athens, Helena Smith reports:

Speaking to a local radio station this morning, Sachinidis said it was important that, two years after the debt crisis erupted in Athens, Greeks realised what was at stake.

The overarching question, he said, was whether Greeks themselves wanted to be in the euro zone. "They [EU nations] want us in but the issue is whether Greeks want to be in the euro zone," he told Flash radio.

"When there are political forces that are saying it won't be so bad to return to the drachma, it is the equivalent of saying we should leave the euro zone. It is our choice, our decision, but if we do that [reject the single currency] we will go back decades. All our achievements will be wiped out and it will happen in such a violent way I don't know if we will be able to continue functioning as a modern democracy."

Those talks have now begun in Athens.

Looking back at Greece, Helena Smith reports that government officials are predicting today that Greece's GDP will have shrunk by almost a third over a five year period by the end of 2012.

That's even worse than the 20% slump that economists have been predicting.

Helena writes:

While the country's official statistics bureau announced on Tuesday that gross domestic product contracted by an annual rate of 6.2% in the first quarter of 2012 – better than the forecast estimate of 6.7% to 7.9% – Greek officials say by the end of the year the downward trajectory will have been dramatic.

"By the close of 2012 we estimate the economy to have shrunk by a total 27% since the start of the recession five years ago," said one official discounting the often-heard figure of 20%. "That's almost a third. It's completely unprecedented for an advanced western economy."

With Athens being asked to enact more austerity measures – including reducing the minimum wage by a further 22% - the process of aggressive internal devaluation would only get worse, the official said.

The slowing up of the recession was attributed to the "stabilising effect" of the recent massive debt restructuring with the country's private sector creditors. The bond exchange had been a precondition of foreign lenders – the EU, ECB and IMF – agreeing to give debt-stricken Greece a second €130bn bailout to cover financing needs through to 2015.

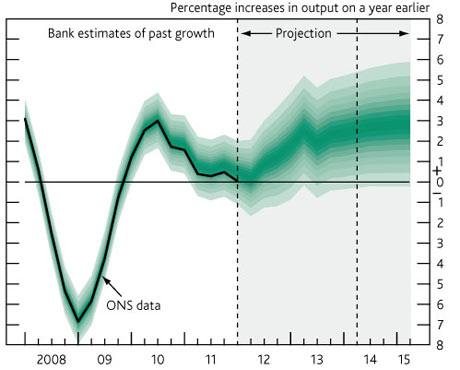

You can see the Bank of England's quarterly inflation report here on its website, in which it explains why UK growth will be lower than expected, and inflation will be higher.

Among other 'highlights', it predicts that UK GDP will be as much as 0.5% lower than would otherwise be the case in the current quarter because of the impact of the Queen's Diamond Jubilee bank holiday in June. That indicates that the British recession will continue for a third quarter.

On the upside, that 'lost activity' should return in Q3 2012.

Mervyn King has urged European policymakers to stop tinkering around the edges of the euro crisis and actually fix the underlying problems.

Governor King said that the most depressing thing about the crisis is that politicians keep treating the crisis as a liquidity problem, when the real crisis is about solvency.

At some point, credit losses need to be recognised and shared around.

Just kicking the can around will not solve the problem.

King also warned that Britain cannot expect to be spared the impact of the Eurozone crisis, at a time when "its biggest trading partner is tearing itself apart" with no clear plan how it will be resolved.

Our banking sector is exposed to the eurozone...and so are our exporters

The Bank of England had a double-dose of bad news for UK citizens today. Not only has the growth forecast been cut this year, to just an 0.8% increase in GDP, it has also admitted that inflation will not fall back to target as quickly as hoped.

This growth chart, from the report, shows how UK GDP could expand, or contract in the years ahead (darker colours=more likely).

Yes, once again, the Bank of England's forecasts have been found wanting. Sir Mervyn King didn't appreciate being asked whether the UK central bank is taking steps to improve its performances -- saying that the key question is whether its forecasts were based on the right data.

Bank of England governor Mervyn King told reporters that contingency plans for the break-up of the eurozone are being discussed between the Bank and the UK government.

King refused to elaborate, saying he wasn't prepared to fan the flames of speculation.

Photograph: Bloomberg TV

Photograph: Bloomberg TV

Sir Mervyn King is warning now that the eurozone crisis is the single biggest threat to Britain's recovery from recession.

Indeed, a disorderly break-up of the eurozone would be so catastrophic that the Bank of England continues to exclude it from its forecasts. But even without it, the Bank now believes that the UK will only grow by around 0.8% this year (down from 1.2% previously).

Speaking as the Bank released its latest quarterly inflation report, Governor King said:

Even the threat of those more extreme outlooks are enough to affect the outlook for the UK.

In other words, UK economic growth is already being hindered by the euro crisis (a pattern which must be repeated in other countries).

Governor King added that Britain continues to navigate through turbulent waters, amid the "risk of a storm heading our way from the Continent".

Ireland's finance minister, Michael Noonan, has weighed in on the crisis this morning.

In an apparent effort to calm nerves, Noonan said he didn't think there was a "guarantee" that Greece would leave the euro.

Noonan added that Greece might benefit from "a referendum" on its future membership of the eurozone – which I think is an acknowledgement of the battleground on which June's general election will be fought. Still ironic, given how former Greek prime minister George Papandreou was bustled out of office after proposing a public vote on the second Greek bailout.

Noonan also admitted that the Greek crisis could also undermine investor confidence in Ireland -- and prevent it returning to the international markets by the end of 2013.

A rumour was briefly swirling this morning that the European Central Bank was holding an emergency meeting to stem the crisis. It's not true.

The ECB's governing council is indeed meeting in Frankfurt, but it's a regular scheduled meeting. Doubtless the Greek crisis will top the agenda, particularly the reports that the withdrawals from Greece's banks is picking up pace (as discussed at 9.30am)

In the UK, the latest unemployment data has shown a surprise fall in the number of people claiming jobless benefit, and the wider number of people out of work.

Here are the top line figures:

The claimant count fell by 13,700 in April, to 1.59 million

The ILO unemployment measure fell by 45,000 in the January-March quarter, to 2.625m, putting the jobless rate at 8.2%.

My colleague Heather Stewart is analysing the data in more detail now....

News in from Greece where our correspondent Helena Smith says there is one silver lining in the clouds that have gathered over the crisis-hit country -- its battered banks are about to receive a much-needed cash injection.

Helena writes:

The news that the EU has given its blessing to the release of €18bn in recapitalization funds for Greeks banks has been met with relief all round in Athens.

Greece's outgoing finance minister Filippos Sachinidis, attending last night's eurozone finance ministers' summit was told the long-awaited cash injection would be disbursed as early as today. And it is not as moment too late, say Greek officials and observers. "The banking system is in dire straits. This is very good news and shows that the EU is following through, it's acting on its promises and that in itself is an act of faith," Nikos Evangelatos, a prominent political commentator told radio listeners this morning.

With all the talk of a Greek exit from the 17-nation euro zone panic-stricken depositors have been rushing to withdraw savings from banks. Since Friday last, an estimated €1bn has been withdrawn from banks according to deeply concerned finance ministry officials. Recapitalisation of the Greek banking system – badly hit by their enforced participation in the country's unprecedented debt restructuring – is a major part of the second €130bn package of rescue loans agreed for Greece earlier this year by the EU, ECB and IMF, its 'troika' of creditors.

News broke yesterday that concerned Greeks had been withdrawing funds since the election of May 6.

Helena also reports that Greek officials are angry that this €18bn injection of funds wasn't released faster:

With the nation's economy effectively on its knees boosting liquidity is seen as the key to kick-starting growth. Apparently the €18bn tranche -- €50bn in total is due -- arrived at the Hellenic Financial Stability Fund (HFSF), an offshoot of the European Financial Stability Fund (EFSF) last week. But after the country's inconclusive elections officials in Brussels refused to release it. "We were furious," said one well-placed official who said the outgoing government had been "preoccupied" with the issue over the past week.

Spanish prime minister Mariano Rajoy was quizzed by journalists in the corridors of the Madrid parliament this morning.

Asked whether the euro could break-up, Rajoy said it would be a ""major error" if Greece were to leave the euro common currency zone.

More as we get it.

Eurosceptic MP Douglas Carswell has declared this morning that all the "damned fools"* who claimed the eurozone would end in disaster have been vindicated.

Conservative parliamentarian Carswell blasted the UK Treasury for supporting the European policy of providing bailouts rather than allowing countries such as Greece to devalue. He claims the single currency risks losing several members - possibly even France.

From this blogpost:

Despite all the evidence to the contrary, the Treasury is still fixated with the idea that the Euro equals prosperity.

The question for the rest of us is no longer Greek Euro membership. It is can Italy, Spain and France remain in a currency union with a German-Austrian-Dutch bloc. And having escaped from Europe's recessionary mechanism, how quickly can our trade partners return to prosperity?

* - it's a quote from 19th century prime minister Lord Melborne, who said on Catholic emancipation in Ireland that "What all the wise men promised has not happened and what all the damned fools said would happen has come to pass".

In the City, traders have driven the FTSE 100 down to its lowest level since December 20, amid talk of the risk of social disorder in Greece, and the risk of contagion spreading to other peripheral countries such as Italy and Spain (whose sovereign debt has come under new pressure - see 8.22am).

Mike McCudden, head of derivatives at Interactive Investor, said many investors were now pulling money out of the stock market in anticipation of Greece leaving the eurozone soon. He added:

In recent months, global markets have been relying on the US and emerging markets such as China to deliver on the global stage, but now that they are stuttering, the ongoing Eurozone issues are hitting the markets harder than ever.Time is running out for the Eurozone to come together and agree on decisive action. With a backdrop of increasing social unrest over austerity measures and signs of cracks in the foundations of the pact amongst the key players, finding the right collective political and economic solution to stem the rot and prevent contagion is looking increasingly unlikely.

Photograph: Reuters

Photograph: Reuters

The FTSE 100 is currently down 61 points at 5376, having lost 10% of its value in the last two months. These are the biggest fallers.

Italy's industry minister has claimed that the eurozone could definitely survive without Greece.

Speaking on a TV news programme this morning, Corrado Passera argued that a Grexit would not be terminal for the single currency. Passera said:

That the euro can continue to exist without Greece is a foregone conclusion.

He also blamed European leaders for pushing the country into such a perilous state, saying:

Europe has been unable to manage Greece's problems in the right way, and now it is making demands from Greece that are probably impossible.

(quotes via Reuters)

There are very worrying signs in the bond markets this morning.

Spanish bond yields* are climbing. They hit a high of 6.52%, and are climbing close to that 7% that marks the 'danger zone' where a country cannot borrow affordably any more.

The spread between French and German bond yields has hit its widest level since early January. That's a sign that traders are treating France's debt as increasingly risky compared to Germany's (the benchmark), and is certainly not good news.

The yield on bonds issued by Greece after its debt swap, which mature in 2023, has just risen above 30%. That suggests a high risk of default.

* - broadly speaking, yields are a measure of the interest rate on a bond; a rising bond yield means the value of the debt has fallen.

The euro is losing value against other currencies too this morning. In early trading it fell to $1.2682, a new four month low.

As feared, European stock markets have opened sharply lower this morning. Banks and mining stocks are being hit hard, as investors across the region raced to sell shares in the face of the turmoil in the eurozone.

In London, the FTSE 100 has shed 75 points to 5365, its lowest level of 2012, and a fall of 1.1%. All but two stocks have fallen. The biggest losers include commodities giant Glencore, and miners Xstrata and Rio Tinto -- reflecting fears that the global economic growth could be crushed by the shockwaves caused if Greece crashed out of the eurozone and defaulted.

Other European markets are hitting their lowest levels for the year – or, in Spain's case, their lowest level since 2003. Here's a round-up:

Spanish IBEX: down 1.8% at 6576

Italian FTSE MIB: down 1.8% at 12062

German DAX: down 0.9%

French CAC: down 0.7%

City analysts agree this morning that Greece is clinging onto its place in the eurozone. Here's a round-up:

Investec:

As it stands the June election results are likely to make abandonment of the bailout programme and a Euro exit more likely.

We shouldn't underestimate the political significance of the EU and its history, but ultimately I do not think the core countries will allow themselves to be 'held hostage' to Greek politics. An exit will inevitably be messy and contagion is a very real issue, but avoiding it may make it very difficult to continue fiscal and economic reforms in the rest of Europe if Greece is seen to get special treatment.

Michael Hewson of CMC Markets

The choice facing Greece voters is the certainty of more spending cuts and austerity until 2020 when it is hoped that the debt to GDP ratio will fall to 120% of GDP or the uncertainty of a sharp brutal default and exit with the possibility, if things do go to plan, of a potential return to growth in two to three years, if reforms are implemented.

If the second election produces a similar result to the first one then it remains unclear how Greece could stay in the euro, a fact acknowledged by IMF chief Christine Lagarde when she said last night that "we have to be technically prepared for anything."

Cameron Peacock of IG Index

We now seem to be back in that 'Groundhog Day ' phase that characterised so much of last year, where European issues (Greece in particular) seemed to trump just about everything else.

Also hurting sentiment towards the shared currency were reports that €700 million of cash deposits had been withdrawn from Greece's major banks in the week and a half since the stalemate election. Some are suggesting that Greek citizens now see 'cash under the mattress' as being a safer option than cash in the bank.

While much of Europe was asleep, Asian shares were falling as the full implications of the crisis hit home. Many markets hit their lowest levels since January.

Andrew Sullivan at Piper Jaffray summed up the mood thus:

Investors are thinking: We don't know what's going to happen with Greece, we don't know what's going to happen with Europe, we're just going to sit it out.

Nikkei 225: down 100, or -1.12%, at 8,801 (closed)

Hang Seng down 631, or -3.17%, at 19,263

Shanghai down 28 points, or -1.13%, at 2,459

S&P ASX down 102 points, or -2.35%, at 4,215

Sensex down 337 points, or -2.06%, at 15,991

Good morning, and welcome to another day of our rolling coverage of the eurozone financial crisis.

Following the collapse of government talks in Greece yesterday, the crisis has entered a new phase. Stock markets have fallen in Asia overnight, with Hong Kong's Hang Seng shedding 3%, and Japan's Nikkei falling 99 points to 8801. Traders expect heavy falls at the start of trading in Europe.

In Greece itself, party leaders are due back at the presidential palace to agree the details of an interim government. It could call elections as early as 10 June, although the 17th appears a more likely date.

It's also a busy day in the UK economy. The latest unemployment data will be released at 9.30am, and an hour later the Bank of England will deliver its quarterly inflation report.

Hold on to your hats ...